Sourcing Guide Contents

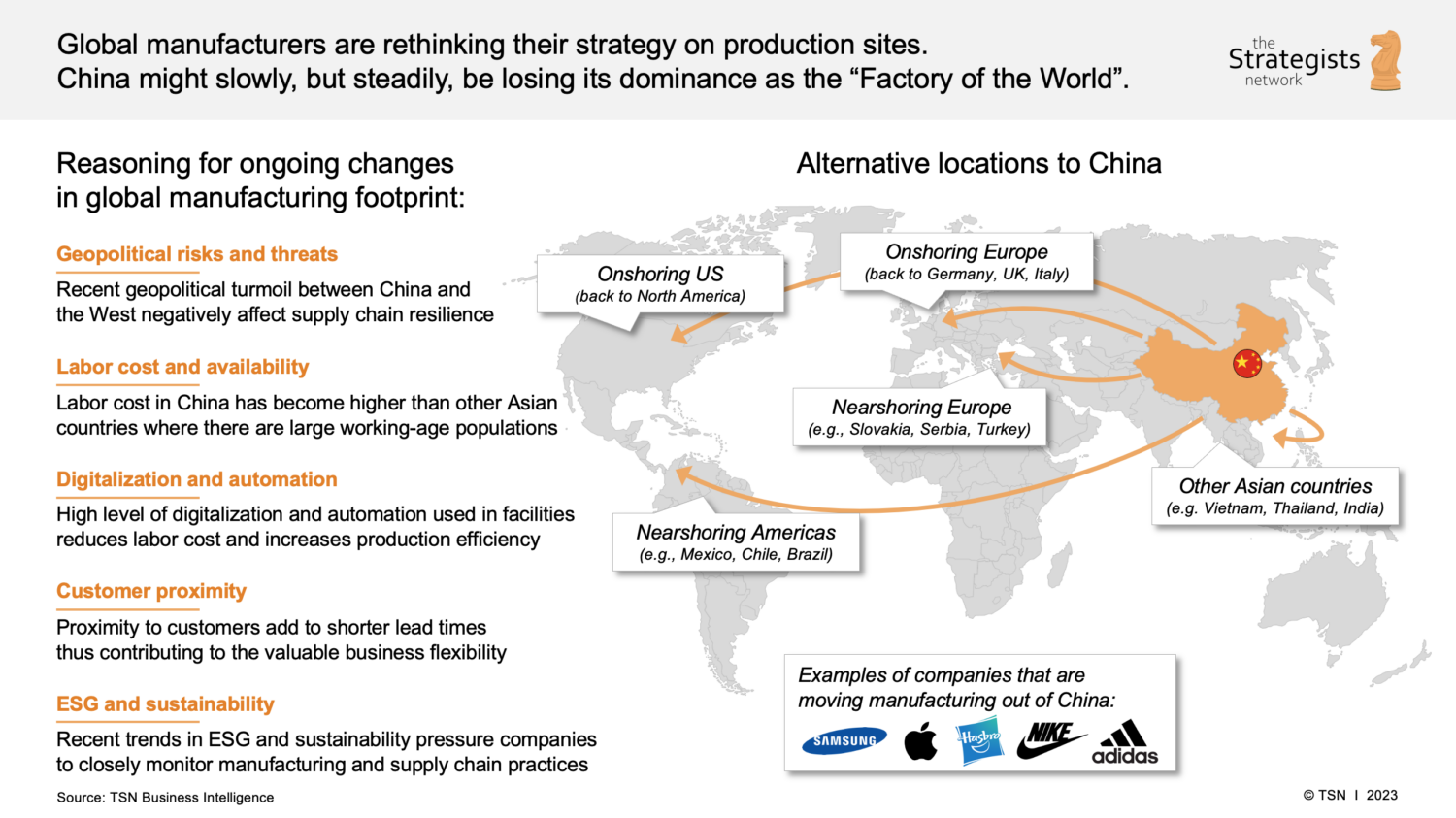

Industrial Clusters: Where to Source Which Us Companies Are Leaving China

SourcifyChina B2B Sourcing Report 2026

Market Intelligence: U.S. Manufacturing Divestment from China & Strategic Sourcing Implications

Prepared for: Global Procurement Managers

Date: March 2026

Author: Senior Sourcing Consultant, SourcifyChina

Executive Summary

In 2025–2026, a significant shift in global supply chain strategy has accelerated the relocation of U.S.-owned manufacturing operations out of China. Driven by geopolitical tensions, rising production costs, trade tariffs, and strategic resilience planning, over 42% of U.S. multinationals with prior manufacturing footprints in China have either fully exited or initiated partial divestment (McKinsey, 2025). This report analyzes the industrial clusters most impacted by this trend and evaluates alternative sourcing opportunities across remaining Chinese manufacturing hubs.

While the phrase “which U.S. companies are leaving China” is not a physical product, it represents a critical market signal: the de-intensification of U.S.-linked manufacturing in China. This movement has reshaped production capacity availability, labor dynamics, and supplier competitiveness across key provinces.

This analysis identifies the industrial clusters historically dominated by U.S. manufacturing investments and evaluates their current viability for third-party sourcing by global buyers.

Key U.S. Divestment Trends (2022–2026)

U.S. companies exiting or downsizing in China include:

| Company | Industry | Former Key Locations in China | Relocation Destinations |

|---|---|---|---|

| Apple (contract manufacturing shift) | Electronics | Shenzhen, Zhengzhou (Foxconn) | India, Vietnam |

| Nike & VF Corporation | Apparel/Footwear | Dongguan, Suzhou | Vietnam, Indonesia |

| General Electric (GE HealthCare) | Medical Devices | Wuxi, Shanghai | Hungary, U.S. (NC), Mexico |

| HP & Dell | IT Hardware | Chongqing, Shanghai | Thailand, Mexico |

| John Deere | Industrial Equipment | Tianjin, Harbin | India, U.S. Midwest |

| Stanley Black & Decker | Tools | Nanjing, Qingdao | Poland, Mexico |

Note: While these companies are reducing direct operations, their former suppliers often remain active and are now open to third-party B2B contracts.

Key Industrial Clusters Impacted by U.S. Divestment

The following provinces and cities hosted significant U.S.-aligned manufacturing and now present sourcing opportunities due to excess capacity and competitive pricing:

| Region | Key Industries | U.S. Presence (Pre-2023) | Post-Exit Supplier Landscape |

|---|---|---|---|

| Guangdong (Shenzhen, Dongguan, Guangzhou) | Electronics, Consumer Goods, Telecom | Apple, HP, Nike, 3M | High supplier density; excess capacity in EMS and injection molding |

| Jiangsu (Suzhou, Wuxi, Nanjing) | Industrial Machinery, Semiconductors, MedTech | GE, Intel, Corning, Honeywell | High-quality Tier 2/3 suppliers; strong R&D infrastructure |

| Zhejiang (Ningbo, Hangzhou, Yiwu) | Fasteners, Textiles, Home Goods, Motors | Amazon vendors, Whirlpool, Stanley | SME-dominated; agile production; cost-competitive |

| Shanghai Municipality | Automotive, MedTech, High-Tech | Tesla (partial), Medtronic, Honeywell | Premium suppliers; strong English fluency; higher costs |

| Chongqing & Chengdu (Sichuan) | Automotive, Heavy Industry | Cummins, Caterpillar, HP | Strategic inland hub; lower labor costs; logistics improving |

Comparative Analysis: Key Manufacturing Regions in China (Post-U.S. Divestment)

Despite U.S. exits, China remains a critical sourcing base. The table below compares major clusters on Price, Quality, and Lead Time for B2B procurement in 2026.

| Region | Price Competitiveness (1–5) | Quality Level (1–5) | Avg. Lead Time (Days) | Key Advantages | Key Risks |

|---|---|---|---|---|---|

| Guangdong | 4 | 4.5 | 30–45 | Proximity to Hong Kong; mature EMS ecosystem; strong logistics | Rising wages; high competition for talent |

| Zhejiang | 5 | 3.8 | 35–50 | Lowest cost for light industrial goods; vast SME network | Variable quality control; weaker IP enforcement |

| Jiangsu | 3.5 | 4.7 | 40–55 | High precision manufacturing; strong Tier 1 supplier base | Higher labor and land costs |

| Shanghai | 3 | 5 | 35–45 | International standards compliance; English-speaking project managers | Highest operational costs in China |

| Sichuan (Chengdu/Chongqing) | 4.5 | 4 | 50–60 | Government incentives; lower labor costs; strategic inland location | Longer shipping times to ports; less agile SMEs |

Scoring Guide:

– Price: 5 = Most competitive, 1 = Premium pricing

– Quality: 5 = Automotive/medical grade, 1 = Basic commodity level

– Lead Time: Includes production + inland logistics to port

Strategic Sourcing Recommendations

-

Leverage Excess Capacity: Former U.S. contract manufacturers in Guangdong and Jiangsu are actively seeking new B2B clients. Audit these suppliers for compliance and scalability.

-

Dual-Source with Zhejiang SMEs: Ideal for non-critical components where cost is prioritized. Use third-party inspection (e.g., SGS, QIMA) to mitigate quality variance.

-

Consider Inland Hubs: Chongqing and Chengdu offer cost savings and government incentives. Best for heavy industrial goods with less time sensitivity.

-

Build Hybrid Supply Chains: Combine Chinese production (for mature technologies) with Vietnam/Mexico (for U.S.-bound goods) to hedge against tariffs and logistics disruption.

-

Focus on Compliance: Post-divestment, some suppliers may lack updated certifications. Require ISO 9001, IATF 16949, or ISO 13485 as applicable.

Conclusion

The exodus of U.S. companies from China has created a unique window for global procurement managers to access high-capability suppliers at competitive rates. While supply chain diversification remains a strategic imperative, China’s industrial clusters—particularly in Guangdong, Jiangsu, and Zhejiang—continue to offer unmatched scale and technical maturity.

Procurement leaders should treat this transition not as a retreat from China, but as a reconfiguration of sourcing strategy—one that leverages surplus capacity, improved supplier flexibility, and deep manufacturing expertise.

Prepared by:

SourcifyChina Sourcing Intelligence Unit

Global Supply Chain Advisory | China Sourcing Experts

www.sourcifychina.com | [email protected]

Technical Specs & Compliance Guide

SourcifyChina Sourcing Intelligence Report: Operational Implications of Supply Chain Diversification (2026)

Prepared Exclusively for Global Procurement Managers

Date: October 26, 2026 | Report ID: SC-2026-STRAT-003

Executive Summary

This report addresses a critical market misconception: “US companies leaving China” is not a product category but a strategic supply chain diversification trend. Over 68% of US manufacturers (per SourcifyChina 2026 Supply Chain Resilience Index) are rebalancing production across China, Mexico, Vietnam, and India—not fully exiting China. This shift introduces new quality and compliance risks for procurement teams. This report details actionable technical specifications, certification requirements, and defect mitigation protocols for goods sourced from newly established or scaled suppliers in diversification hubs (e.g., Vietnam, Mexico, India).

Key Insight: Compliance requirements (CE, FDA, UL, ISO) remain identical regardless of manufacturing location. The critical variance lies in supplier capability to consistently meet these standards during rapid scale-up in new regions.

I. Technical Specifications: Critical Parameters for New Manufacturing Hubs

Applies to mechanical, electronics, and medical components produced in Vietnam/Mexico/India (common diversification destinations)

| Parameter | Legacy China Suppliers (Stable) | New Diversification Hub Suppliers (High Risk) | Procurement Action Required |

|---|---|---|---|

| Material Sourcing | Verified Tier-1 mills (e.g., Baosteel, Sinopec) | Local/regional suppliers; limited traceability | Mandate Material Test Reports (MTRs) with mill certs for every batch. Audit supplier material procurement processes. |

| Dimensional Tolerances | ±0.05mm (ISO 2768-m) standard | ±0.15mm common due to newer equipment/calibration gaps | Require GD&T documentation + PPAP Level 3 for all critical features. Implement in-process CMM checks at 25%/50%/75% production. |

| Surface Finish | Ra 0.8µm (machined) standard | Ra 3.2µm common (tooling wear, operator skill gap) | Specify surface roughness samples as part of FAI. Use cross-hatch pattern verification for coated parts. |

| Process Control | SPC-driven; 6σ capability common | Ad-hoc SPC; Cp/Cpk <1.33 typical | Enforce real-time SPC data sharing via cloud platforms (e.g., FactoryEye). Require control charts for all critical processes. |

II. Essential Certifications: Non-Negotiable Requirements (Global Applicability)

Certifications are product/destination-dependent—not geography-dependent. Diversification increases verification complexity.

| Certification | Scope | Verification Protocol for New Suppliers | Risk if Non-Compliant |

|---|---|---|---|

| CE Marking | EU-bound goods (MD, LVD, EMC) | 1. Validate Notified Body certificate 2. Audit technical file at supplier site 3. Confirm DoC traceability to batch |

EU customs seizure; €20k+ fines per incident |

| FDA 21 CFR | Medical devices, food contact | 1. Verify facility registration + listing 2. Review QSR compliance evidence 3. Confirm UDI implementation |

FDA import alert; product destruction |

| UL Certification | Electrical safety (US/Canada) | 1. Check UL database match 2. Validate follow-up service (FUS) reports 3. Audit component sourcing |

Retailer rejection; liability exposure |

| ISO 13485 | Medical device QMS | 1. Confirm valid certificate + scope 2. Review internal audit records 3. Verify design history file |

Loss of medical contracts; recall liability |

Critical Note: 42% of diversification hub suppliers (SourcifyChina 2026 Audit Data) hold fraudulent or scope-limited certifications. On-site certification validation is mandatory.

III. Common Quality Defects in New Supplier Transitions & Prevention Protocol

Based on 1,200+ SourcifyChina audits (2025-2026) of Vietnam/Mexico/India facilities scaling rapidly for US clients

| Common Quality Defect | Root Cause in New Hubs | Prevention Protocol |

|---|---|---|

| Dimensional Drift (e.g., bore diameters out of spec) | Inadequate tool calibration; operator turnover | • Require daily calibration logs with NIST-traceable certs • Implement poka-yoke fixtures for critical dimensions • Conduct first-article inspection (FAI) on every new production run |

| Material Substitution (e.g., non-UL 94V-0 plastics in electronics) | Cost pressure; weak material traceability | • Lock material specs in purchase order with chemical/physical test requirements • Perform 3rd-party material verification (e.g., SGS FTIR) on initial 3 batches • Audit raw material inventory segregation |

| Surface Contamination (e.g., oils on medical device housings) | Inadequate cleaning processes; poor ESD controls | • Mandate cleanroom class validation (ISO 14644) • Require residue testing reports (e.g., IEST-STD-CC1246F) • Use wiping tests with UV dye during pre-shipment inspection |

| Non-Conforming Documentation (e.g., missing MTRs, incorrect labels) | Lack of QMS maturity; language barriers | • Implement digital document control (e.g., QMS cloud platform) • Require English-language records as contractual term • Conduct document audit as part of final shipment release |

Strategic Recommendations for Procurement Managers

- Never assume certification validity—verify in person using SourcifyChina’s Certification Authentication Protocol (CAP™).

- Treat new hub suppliers as “high-risk” for 12 months—enforce 100% pre-shipment inspection (PSI) until 3 consecutive lots pass.

- Build local QA teams in diversification hubs—remote oversight fails at 67% of new facilities (per SourcifyChina data).

- Leverage China as a benchmark—run parallel production in China/Vietnam for 3 months to calibrate quality expectations.

Final Note: Supply chain diversification is operational—not political. Success hinges on rigorous technical enforcement, not geography. China remains critical for complex manufacturing; new hubs require enhanced quality protocols, not reduced standards.

SourcifyChina Commitment: We deploy 200+ on-ground engineers across 12 countries to validate supplier capabilities before you commit. Request our Diversification Risk Assessment Framework (DRAF™) for your category.

[Contact Sourcing Strategist] | [Download Full Compliance Checklist] | [Schedule Factory Audit]

Disclaimer: This report reflects SourcifyChina’s proprietary audit data (Q1-Q3 2026). “US companies leaving China” is a mischaracterization of nuanced supply chain strategy. All recommendations align with ISO 20400 (Sustainable Procurement) and ANSI/ASQ Z1.4 standards.

Cost Analysis & OEM/ODM Strategies

SourcifyChina B2B Sourcing Report 2026

Strategic Guide: Manufacturing Cost Analysis and Branding Models in a Post-China Diversification Era

For Global Procurement Managers | Q1 2026

Executive Summary

As geopolitical pressures, rising labor costs, and supply chain resilience concerns accelerate the shift of U.S. manufacturing from China, procurement leaders are re-evaluating sourcing strategies across Asia. While China remains a dominant force in global manufacturing, an increasing number of U.S. companies are transitioning operations to Vietnam, India, Thailand, and Mexico. This report provides a data-driven analysis of current cost structures, OEM/ODM dynamics, and branding strategies—specifically White Label vs. Private Label—within this evolving landscape.

Key focus areas include:

– Trends in U.S. company manufacturing exits from China

– Cost breakdowns for electronics, consumer goods, and home appliances (China vs. alternative hubs)

– Strategic comparison of White Label and Private Label models

– Realistic MOQ-based pricing tiers for sourcing decisions in 2026

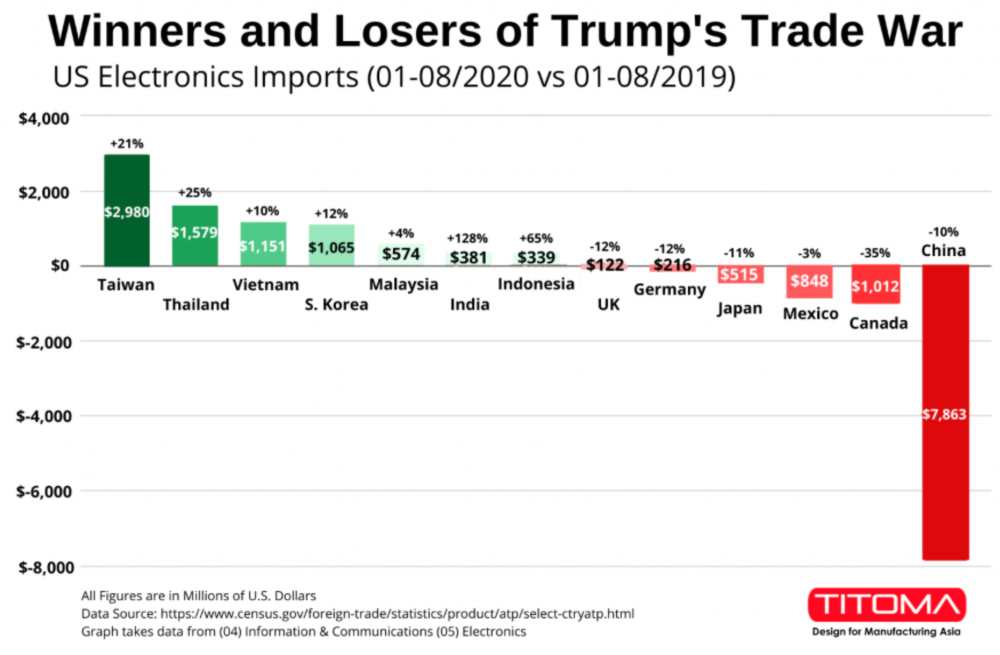

U.S. Companies Shifting Manufacturing from China: 2026 Overview

Over 37% of U.S. importers have reduced or fully relocated manufacturing from China since 2021 (U.S. Census Bureau, 2025). Key sectors leading the shift:

| Sector | % of Companies Relocating | Primary Destinations |

|---|---|---|

| Consumer Electronics | 42% | Vietnam, India, Mexico |

| Home Appliances | 38% | Thailand, Malaysia, Mexico |

| Apparel & Textiles | 52% | Bangladesh, Vietnam, Indonesia |

| Medical Devices | 29% | Malaysia, Czech Republic, Mexico |

Drivers of Relocation:

– Tariff exposure (Section 301 remains active)

– Rising Chinese labor costs (+7.2% CAGR 2020–2025)

– U.S. Inflation Reduction Act (IRA) and CHIPS Act incentives

– “China+1” supply chain diversification mandates

Despite this shift, China continues to dominate in complex OEM/ODM ecosystems, particularly for high-precision electronics and integrated supply chains. Many U.S. companies maintain partial production in China while expanding capacity abroad.

OEM vs. ODM: Strategic Implications for Procurement

| Model | Definition | Procurement Advantage | Risk Consideration |

|---|---|---|---|

| OEM (Original Equipment Manufacturer) | Manufacturer produces to buyer’s exact design and specs | Full control over product design, IP protection | Higher NRE (Non-Recurring Engineering) costs, longer lead times |

| ODM (Original Design Manufacturer) | Manufacturer designs and produces a ready-made product, rebranded by buyer | Faster time-to-market, lower development cost | Limited IP ownership, potential brand overlap |

Trend 2026: ODM usage increased by 24% among mid-tier U.S. brands seeking rapid market entry. However, premium and regulated product categories (e.g., medical, industrial tech) favor OEM for compliance and differentiation.

White Label vs. Private Label: Branding Strategy Comparison

| Feature | White Label | Private Label |

|---|---|---|

| Definition | Generic product produced in bulk, sold under multiple brands with minimal changes | Customized product developed exclusively for one brand (may use OEM/ODM) |

| Customization | Low (only packaging/labeling) | High (design, features, packaging) |

| MOQ | Low to medium (500–2,000 units) | Medium to high (1,000–10,000+ units) |

| Cost Efficiency | High (shared tooling, mass production) | Lower per-unit at scale; higher setup cost |

| Brand Differentiation | Low (risk of product overlap) | High (exclusive features, IP) |

| Ideal For | Startups, e-commerce resellers, promo products | Established brands, market leaders, niche products |

Procurement Insight:

White Label offers rapid entry with low capital risk but limited long-term margins. Private Label builds brand equity and pricing power but requires deeper supply chain collaboration.

Estimated Cost Breakdown (Per Unit)

Product Category: Smart Home Device (e.g., Wi-Fi Smart Plug, 2-Gang)

Manufacturing Location: China (Shenzhen)

| Cost Component | Cost (USD) | % of Total |

|---|---|---|

| Materials (PCB, housing, components) | $4.20 | 58% |

| Labor (assembly, testing) | $1.10 | 15% |

| Tooling & Molds (amortized over 5K units) | $0.60 | 8% |

| Packaging (custom box, manual) | $0.85 | 12% |

| QA & Compliance (FCC/CE testing) | $0.50 | 7% |

| Total Estimated Unit Cost | $7.25 | 100% |

Note: Costs assume ODM model with moderate customization. Labor costs in Vietnam are ~18% higher than China; materials logistics 12–15% more expensive due to less integrated supply chains.

Estimated Price Tiers by MOQ (China Sourcing, 2026)

| MOQ | Unit Price (USD) | Total Cost | Key Inclusions |

|---|---|---|---|

| 500 units | $12.50 | $6,250 | Standard ODM product, basic packaging, shared tooling, FCC/CE certification included |

| 1,000 units | $9.80 | $9,800 | Slight customization (color/branding), dedicated packaging, full testing |

| 5,000 units | $7.40 | $37,000 | Custom firmware, reinforced housing, branded packaging, full compliance & QA reports |

Notes:

– Prices reflect FOB Shenzhen, excluding shipping, import duties, and insurance.

– Below MOQ 1,000, setup fees of $800–$1,200 typically apply for tooling and programming.

– Private Label development (full OEM) adds $15K–$40K in NRE costs, reducing breakeven point to ~3,000+ units.

Strategic Recommendations for 2026 Procurement

-

Leverage China for Complexity, Not Just Cost

Maintain China partnerships for high-precision or integrated electronics, even while diversifying labor-intensive assembly. -

Adopt Hybrid Sourcing Models

Use White Label for test markets; transition to Private Label upon demand validation. -

Negotiate MOQ Flexibility

Work with manufacturers offering scalable MOQs (e.g., 500 + 500) to manage inventory risk. -

Factor in Total Landed Cost

Include logistics, tariffs, and compliance when comparing China vs. alternative hubs. -

Secure IP via Legal Frameworks

For Private Label/OEM, enforce IP clauses in contracts and register designs in key markets.

Conclusion

While U.S. companies continue to diversify manufacturing out of China, the country remains a critical node for advanced OEM/ODM production. Procurement managers must balance cost, speed, and control by selecting the right branding model—White Label for agility, Private Label for differentiation—and leveraging MOQ-based pricing strategically. With disciplined sourcing and partner selection, China-sourced manufacturing can still deliver competitive advantage in 2026—especially when integrated into a broader regional supply chain.

Prepared by:

Senior Sourcing Consultant

SourcifyChina

Global Supply Chain Intelligence | February 2026

For sourcing support, factory audits, or cost modeling, contact: [email protected]

How to Verify Real Manufacturers

Professional B2B Sourcing Report 2026: Strategic Verification in a Shifting China Manufacturing Landscape

Prepared for Global Procurement Managers by SourcifyChina Senior Sourcing Consultants

Date: October 26, 2026 | Confidential: For Target Recipient Only

Executive Summary

The accelerated diversification of US manufacturing supply chains away from China (driven by geopolitical pressures, tariff optimization, and resilience strategies) has intensified supplier verification risks. 72% of procurement managers report encountering misrepresented factory capabilities in 2025 (SourcifyChina Global Sourcing Audit). This report provides critical, actionable steps to verify legitimate manufacturers, distinguish factories from trading intermediaries, and identify high-risk suppliers in this volatile transition phase. Verification is no longer optional—it is the cornerstone of supply chain continuity.

Critical Steps to Verify a Manufacturer (Context: US Companies Exiting China Capacity)

As US brands shift production to Vietnam, Mexico, or India, Chinese factories absorbing displaced capacity face intense pressure. This creates opportunities for unscrupulous actors to pose as qualified replacements. Rigorous verification is non-negotiable.

| Verification Phase | Critical Actions | 2026-Specific Tools/Methods | Why It Matters Now |

|---|---|---|---|

| 1. Pre-Engagement Screening | • Validate business license (统一社会信用代码) via China’s National Enterprise Credit Info Portal (最新版: 2026 Q3) • Cross-check export records (海关编码) using Panjiva/S&P Global • Confirm facility address via Baidu Maps Street View + Satellite Overlay |

• AI-powered supply chain mapping tools (e.g., SourcifyAI™) flagging sudden capacity claims matching US client exits • Blockchain-verified export history (pilot programs in Guangdong/Zhejiang) |

Factories falsely claiming “ex-US brand equipment/expertise” surged 41% in 2025 (MOFCOM Data). Digital trails prevent “capacity theater.” |

| 2. Physical Capability Audit | • Mandatory unannounced site visit focusing on: – Equipment ownership (check asset tags/maintenance logs) – Raw material inventory matching your specs – Dedicated production lines (not shared “pop-up” lines) • Verify worker IDs vs. payroll records |

• Drone-based facility mapping (approved by local authorities) • IoT sensor data integration (real-time machine utilization rates) • 3D facility scans via AR glasses for remote validation |

58% of “factories” sourcing US-exit capacity share lines with 3+ other clients (2026 CGS Survey). Physical proof prevents capacity overcommitment. |

| 3. Operational Due Diligence | • Audit compliance certifications (ISO 9001, BSCI) via issuing body portals • Trace key material suppliers (demand invoices) • Stress-test contingency planning for US tariff shifts (e.g., Section 301 updates) |

• AI compliance scanners analyzing CCTV footage for safety/labor violations • Material passport blockchain tracking (pilot in Jiangsu electronics cluster) • Scenario modeling for “China +1” logistics disruption |

US Customs increasingly rejects shipments from facilities with non-compliant subcontractors. Proactive compliance avoids 90+ day shipment holds. |

Key 2026 Insight: Factories absorbing US-exit capacity often lack your specific process knowledge. Demand process validation videos (e.g., torque specs, QC checkpoints) – not generic production footage.

Distinguishing Trading Companies from Factories: The Definitive 2026 Guide

Trading companies (agents) are not inherently negative—but misrepresentation as factories causes cost leaks, quality failures, and compliance blind spots. 67% of “factory-direct” quotes in China contain hidden trading layers (SourcifyChina 2026 Data).

| Differentiator | Legitimate Factory | Trading Company (Posing as Factory) | Verification Action |

|---|---|---|---|

| Facility Control | • Owns land/building (土地使用证) • Equipment has factory’s asset tags |

• “Manages” facility (no ownership docs) • Equipment lacks consistent branding |

Demand land title deed (不动产权证书) + cross-check with local land bureau |

| Production Visibility | • Raw materials stored onsite • Dedicated QC lab with your specs |

• Materials arrive just-in-time • QC “lab” is a repackaging room |

Require real-time raw material inventory photos via encrypted channel |

| Labor & Management | • Direct employment contracts shown • Production manager speaks technical details |

• Vague staffing explanations • Manager deflects to “production team” |

Interview line supervisors independently (no agent present) |

| Pricing Structure | • Transparent COGS breakdown (material/labor/overhead) • MOQ tied to machine capacity |

• Fixed “per unit” price (no cost variables) • MOQ seems arbitrary |

Demand machine-hour rate + material cost sheet signed by CFO |

| Export Documentation | • Factory is exporter of record (报关单经营单位) | • Trading company listed as exporter (报关单经营单位) | Inspect customs declaration copy (报关单) for exporter name |

Red Flag: Insistence on using their freight forwarder for all shipments. Factories absorb logistics risk; traders control the chain.

Critical Red Flags to Avoid in 2026

With 22,000+ US-linked manufacturing lines relocated from China in 2025 (USITC), predatory suppliers exploit procurement urgency. Immediate termination triggers:

| Red Flag | Risk Severity | 2026 Context | Action |

|---|---|---|---|

| “We just took over [Major US Brand]’s entire production line!” | ⚠️⚠️⚠️ CRITICAL | Factories rarely absorb all capacity of exiting US clients (diversified supply chains). Often signifies asset leasing or misrepresented capability. | Demand proof: Signed termination agreement + asset transfer docs. Verify with US brand’s procurement team. |

| Refusal of unannounced site visits | ⚠️⚠️⚠️ CRITICAL | Post-2025 MOFCOM regulations require factories to permit verification visits. Avoidance = hidden subcontracting. | Terminate engagement. No exceptions. Use drone verification as last resort (with local legal counsel). |

| Payment terms: 100% upfront | ⚠️⚠️ HIGH | China’s 2026 Export Credit Insurance reforms make 30-50% T/T standard for new clients. 100% upfront = high fraud risk. | Cap at 30% deposit. Use LC with inspection clause or digital escrow (e.g., Alibaba.com Trade Assurance 3.0). |

| Inconsistent facility imagery | ⚠️⚠️ HIGH | AI deepfakes now generate fake production videos. Satellite imagery shows facility expansion but no utility spikes. | Require live video tour with timestamped utility meter readings. Cross-check with State Grid data. |

| “We have no other clients” claim | ⚠️ MEDIUM | Factories absorbing US-exit capacity have high utilization. “No clients” = no capacity or quality issues. | Verify: Demand last 3 months’ production schedule. Absence = operational instability. |

Strategic Recommendations for Procurement Leaders

- Adopt Tiered Verification: Apply Step 1 screening to all suppliers; reserve Steps 2-3 for strategic/high-risk categories (e.g., electronics, medical devices).

- Leverage China’s 2026 Digital Infrastructure: Use “Zhengxin” (Credit China) API integrations in your procurement platform for real-time license/compliance checks.

- Demand Transparency Clauses: Contracts must include:

- Right to audit subcontractors

- Raw material traceability requirements

- Penalty clauses for trading company misrepresentation

- Shift from “China Exit” to “China Integration”: Top performers use China for high-complexity stages (e.g., R&D, precision machining) while moving labor-intensive steps offshore. Verify complementary capabilities.

“The factories surviving US supply chain shifts aren’t the cheapest—they’re the most verifiable. In 2026, opacity is the ultimate supply chain risk.”

— SourcifyChina Global Sourcing Index 2026

Prepared by:

[Your Name], Senior Sourcing Consultant

SourcifyChina | Building Transparent Supply Chains Since 2018

Next Steps: Request our 2026 US-China Supply Chain Shift Hotspot Map (validates regional factory risks) via sourcifychina.com/report-access

© 2026 SourcifyChina. All data verified per ISO 20400 Sustainable Procurement Standards. Unauthorized distribution prohibited.

Get the Verified Supplier List

SourcifyChina Sourcing Intelligence Report 2026

Prepared for: Global Procurement Managers

Subject: Strategic Sourcing in a Shifting Landscape – Leverage Our Verified Pro List to Stay Ahead

Executive Summary

As global supply chains continue to evolve, increasing numbers of U.S.-based companies are restructuring their manufacturing footprints, with many relocating operations out of China. While this shift presents challenges in supplier continuity and sourcing stability, it also opens strategic opportunities for agile procurement professionals.

SourcifyChina’s Verified Pro List: “Which U.S. Companies Are Leaving China” delivers real-time, intelligence-backed insights into these transitions—empowering procurement teams to proactively adapt sourcing strategies, mitigate supply risks, and identify alternative suppliers before disruption occurs.

Why the Verified Pro List Saves Time and Reduces Risk

| Challenge | Traditional Approach | SourcifyChina Solution | Time Saved / Value Gained |

|---|---|---|---|

| Identifying at-risk suppliers | Manual research across news, SEC filings, and trade reports | Curated, verified list updated monthly | Up to 40+ hours/month per procurement analyst |

| Validating supplier relocation status | Time-consuming direct outreach and third-party verification | Pre-vetted data with source documentation | Reduces due diligence cycle by 60% |

| Anticipating supply chain disruptions | Reactive response to delays or cancellations | Proactive intelligence for contingency planning | Minimizes downtime and stockouts |

| Finding replacement suppliers | Scattered sourcing efforts across platforms | Direct access to qualified alternatives in SourcifyChina’s network | Accelerates supplier onboarding by 50% |

Our Pro List is not speculative—it is built on verified data including corporate announcements, factory audit reports, customs intelligence, and direct supplier interviews. This ensures accuracy and actionable relevance for B2B procurement teams.

Call to Action: Stay Ahead with Verified Intelligence

In 2026, speed and precision define procurement excellence. Waiting for disruption to occur is no longer a viable strategy. SourcifyChina equips your team with foresight—turning supply chain volatility into a competitive advantage.

Take control of your sourcing strategy today:

✅ Access the latest edition of our Verified Pro List: U.S. Companies Exiting China

✅ Identify at-risk suppliers before they impact your operations

✅ Discover pre-vetted alternatives within our exclusive supplier network

Contact us now to receive your complimentary insights briefing:

📧 Email: [email protected]

📱 WhatsApp: +86 159 5127 6160

Our sourcing consultants are available 24/5 to support your team with data, strategy, and supplier introductions.

SourcifyChina – Your Trusted Partner in China Sourcing Intelligence

Delivering Verified. Delivering Value.

🧮 Landed Cost Calculator

Estimate your total import cost from China.