Sourcing Guide Contents

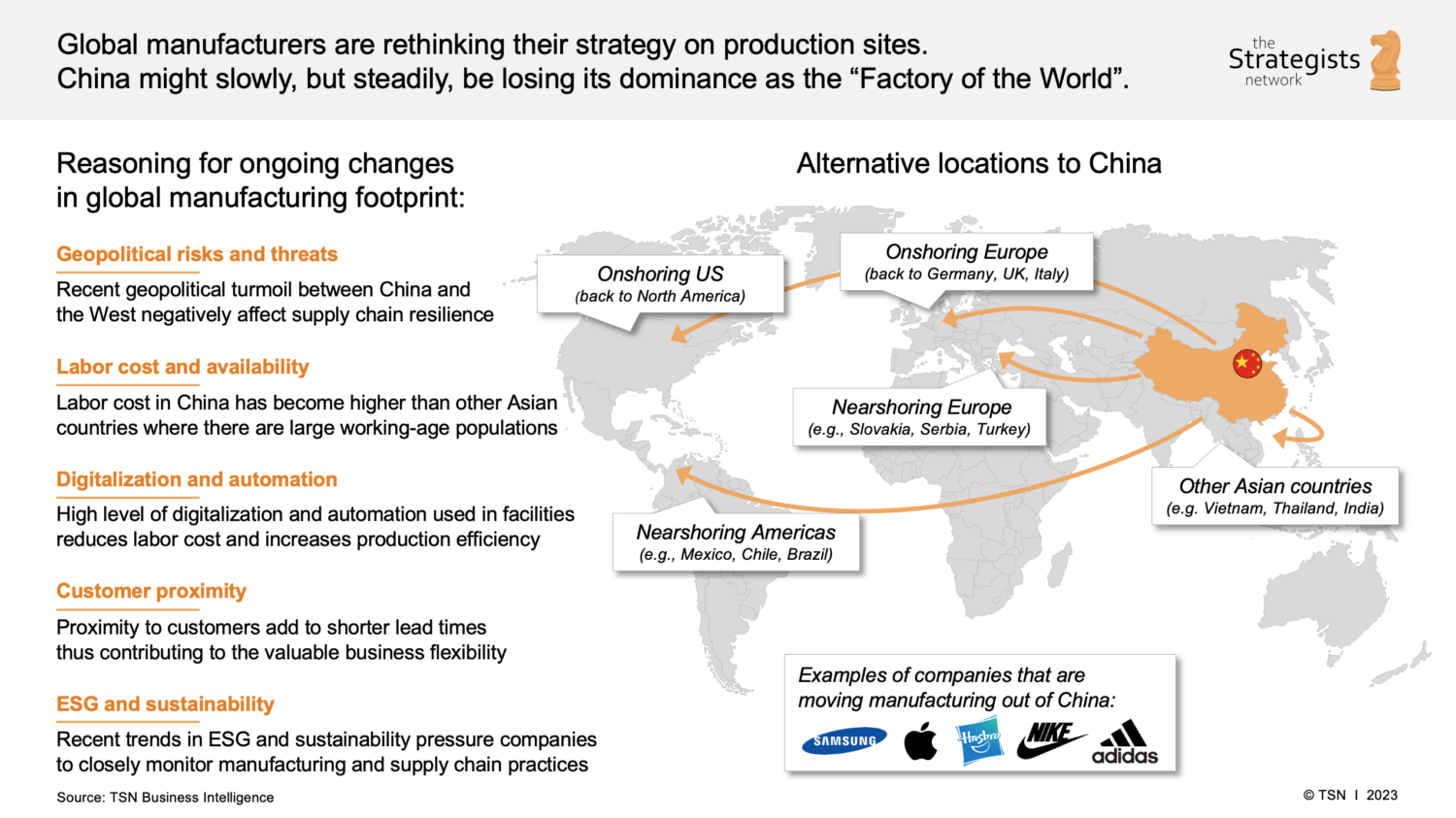

Industrial Clusters: Where to Source What Companies Are Leaving China

SourcifyChina

B2B Sourcing Intelligence Report 2026

Title: Market Realignment in Chinese Manufacturing: Sourcing Strategy in the Era of Industrial Relocation

Prepared For: Global Procurement Managers

Date: Q1 2026

Author: Senior Sourcing Consultant, SourcifyChina

Executive Summary

Contrary to the narrative of a wholesale exodus, the manufacturing landscape in China is undergoing strategic realignment rather than mass abandonment. While certain multinational corporations and labor-intensive sectors are relocating portions of their supply chains to Vietnam, India, Mexico, and Southeast Asia, China remains the world’s largest manufacturing hub—accounting for 30% of global output (UNIDO, 2025). The shift is not about “leaving China” entirely but rebalancing capacity due to rising costs, geopolitical pressures, and supply chain resilience strategies.

This report analyzes the geographic footprint of industrial relocation trends, identifies key manufacturing clusters still dominant in production, and provides a comparative assessment of core industrial provinces to guide procurement decisions in 2026 and beyond.

Section 1: Understanding the “Leaving China” Narrative

The phrase “what companies are leaving China” oversimplifies a complex transition. The following trends define the current environment:

- Sector-Specific Movement: Labor-intensive industries (e.g., basic textiles, footwear, low-end electronics assembly) are most affected.

- Partial Relocation: Most companies adopt a China+1 or China+N strategy, maintaining high-value manufacturing in China while shifting volume production abroad.

- Geopolitical Drivers: U.S. tariffs, EU CBAM, and technology restrictions accelerate diversification, but not full exits.

- Domestic Upgrading: China is incentivizing high-tech, automation, and green manufacturing—phasing out low-margin industries.

Insight: China’s manufacturing GDP grew by 5.2% in 2025 (NBS), outpacing global average, indicating continued industrial strength despite restructuring.

Section 2: Key Manufacturing Clusters and Relocation Trends by Region

The following provinces and cities represent China’s core industrial ecosystems. While some face outflows, they remain critical for high-complexity, high-quality production.

| Province/City | Key Industrial Clusters | Industries Affected by Outflow | Industries Strengthening | Relocation Pressure Level |

|---|---|---|---|---|

| Guangdong (Pearl River Delta) | Shenzhen, Dongguan, Guangzhou, Foshan | Consumer electronics assembly, textiles, basic plastics | AI hardware, EV components, robotics, smart devices | High |

| Zhejiang (Yangtze River Delta) | Hangzhou, Ningbo, Yiwu, Wenzhou | Low-end hardware, seasonal apparel | E-commerce fulfillment, precision machinery, green tech | Medium |

| Jiangsu | Suzhou, Wuxi, Nanjing | Legacy automotive parts, basic chemicals | Semiconductor packaging, biopharma, new materials | Medium |

| Shanghai | Pudong, Songjiang | Labor-intensive final assembly | R&D centers, high-end medtech, automation systems | Low |

| Sichuan/Chongqing | Chengdu, Chongqing | None significant | Aerospace, EV battery production, data centers | Low (growing in) |

| Fujian | Xiamen, Quanzhou | Footwear, sportswear (e.g., Nike, Adidas suppliers) | Solar PV, marine equipment | High |

Note: Relocation pressure is highest in Guangdong and Fujian due to proximity to export ports and reliance on export-oriented, labor-heavy models.

Section 3: Comparative Analysis of Key Manufacturing Regions

The table below evaluates China’s top sourcing regions based on Price, Quality, and Lead Time—critical KPIs for procurement strategy.

| Region | Price Competitiveness | Quality Consistency | Average Lead Time (Days) | Best For | Risk Factors |

|---|---|---|---|---|---|

| Guangdong | ⭐⭐⭐☆ (Moderate) | ⭐⭐⭐⭐⭐ (Excellent) | 25–35 | High-tech electronics, precision components, fast-turnaround OEM | Rising labor costs, high competition for capacity |

| Zhejiang | ⭐⭐⭐⭐ (Strong) | ⭐⭐⭐⭐ (Very Good) | 30–40 | Hardware, textiles, e-commerce goods, machinery | Fragmented SME base, variable QC in low-cost zones |

| Jiangsu | ⭐⭐⭐☆ (Moderate) | ⭐⭐⭐⭐⭐ (Excellent) | 30–35 | Semiconductors, chemicals, automotive subsystems | Regulatory tightening on emissions |

| Shanghai | ⭐⭐☆ (Low) | ⭐⭐⭐⭐⭐ (Premium) | 35–45 | R&D-driven manufacturing, medical devices, automation | High costs, limited volume capacity |

| Sichuan/Chongqing | ⭐⭐⭐⭐☆ (Very Strong) | ⭐⭐⭐☆ (Good) | 40–50 | Heavy industrial parts, EV batteries, aerospace | Longer logistics to ports, less supplier density |

Legend: ⭐ = Low, ⭐⭐ = Moderate, ⭐⭐⭐ = Competitive, ⭐⭐⭐⭐ = Strong, ⭐⭐⭐⭐⭐ = Excellent

Section 4: Strategic Implications for Global Procurement

1. Do Not Abandon China—Optimize Within

China remains unmatched in supply chain density, engineering talent, and scale. The goal is not exit, but strategic specialization:

– Source high-complexity, innovation-driven products from Guangdong, Jiangsu, and Shanghai.

– Use Zhejiang and Sichuan for cost-sensitive but quality-assured volume production.

2. Monitor Secondary Sourcing Hubs

While Vietnam and India absorb displaced capacity, they lack China’s ecosystem maturity. Use them for modular assembly, not full product development.

3. Leverage Automation to Offset Labor Shifts

Factories in Guangdong and Jiangsu are investing heavily in automation (Industry 4.0 adoption up 40% since 2022). This mitigates labor cost pressure and improves lead time predictability.

4. Compliance & Resilience

Procurement strategies must account for:

– Dual-use technology restrictions

– Carbon footprint reporting (CBAM readiness)

– Local content requirements in target markets

Conclusion

The narrative of “companies leaving China” reflects selective repositioning, not systemic decline. Industrial clusters in Guangdong, Zhejiang, and Jiangsu continue to dominate global manufacturing, particularly in high-value sectors. While cost pressures drive some capacity overseas, China’s upgraded industrial base offers unparalleled quality, speed, and technical capability.

Recommendation: Maintain China as a core sourcing pillar, but adopt a tiered regional strategy—leveraging each province’s strengths while building complementary capacity in alternative markets for risk mitigation.

Appendix: Sourcing Action Plan 2026

| Action | Timeline | Objective |

|---|---|---|

| Audit current China suppliers by region and capability tier | Q1 2026 | Identify exposure to high-pressure zones |

| Qualify 1–2 suppliers in Sichuan/Chongqing for EV/industrial components | Q2 2026 | Diversify inland, lower-cost options |

| Develop dual-sourcing with Vietnam/Mexico for labor-intensive lines | Q3 2026 | Build resilience without sacrificing quality |

| Implement AI-driven supplier performance tracking | Ongoing | Monitor lead time, defect rates, compliance |

Prepared by:

Senior Sourcing Consultant

SourcifyChina — Global Supply Chain Intelligence

Empowering Procurement Leaders with Data-Driven Sourcing Strategies

© 2026 SourcifyChina. Confidential. For internal procurement use only.

Technical Specs & Compliance Guide

Professional B2B Sourcing Report 2026: Navigating Supply Chain Diversification Beyond China

Prepared for Global Procurement Managers | SourcifyChina Senior Sourcing Consultants

Date: October 26, 2026 | Confidential: For Client Strategic Planning Only

Executive Summary

Contrary to popular narrative, companies are not “leaving China” but strategically diversifying supply chains to mitigate geopolitical, logistical, and cost volatility. China remains a critical manufacturing hub (42% of global exports, WTO 2025), but procurement leaders now adopt a “China +1/N” model. This report details technical and compliance imperatives for managing quality during supply chain transitions, focusing on factories relocating production to Vietnam, Mexico, India, and Thailand. Success hinges on rigorous adherence to specifications and certifications – not geographic origin.

I. Technical Specifications & Compliance: Non-Negotiables for Transitioning Suppliers

Compliance requirements are product/category-specific and DO NOT change based on manufacturing location. Diversification amplifies enforcement risk.

Key Quality Parameters

| Parameter | Critical Requirements | Risk During Transition |

|---|---|---|

| Materials | • Traceable mill/test certificates (e.g., ASTM A36 for steel, UL 94 for plastics) • Zero tolerance for substitution without written approval |

New suppliers may use inferior local materials to cut costs; undocumented “equivalent” substitutions common |

| Tolerances | • GD&T (Geometric Dimensioning & Tolerancing) compliance per ISO 1101 • Critical features: ±0.05mm (precision machining), ±0.1mm (stamping) |

Inconsistent metrology calibration in new facilities; lack of skilled CMM operators |

Essential Certifications (Product-Dependent)

Certifications follow the product, NOT the factory location. Relocation requires re-validation.

| Certification | Scope | Transition Compliance Requirement | Common Gap in New Locations |

|---|---|---|---|

| CE | EU Machinery/EMC/LVD Directives | Full Technical File audit + EU Authorized Representative appointment | Incomplete DoC; missing harmonized EN standards |

| FDA 21 CFR | Medical devices, food contact surfaces | QSR-compliant facility audit + Device Master Record validation | Lack of QMS documentation; inadequate sterilization controls |

| UL | Electrical safety (US/Canada) | Factory Follow-Up Services (FUS) inspection + certified component list | Substituted non-UL components; counterfeit marks |

| ISO 9001:2015 | Quality Management System | Full scope certification + management review evidence | Paper-only systems; no internal audit rigor |

Critical Insight: 68% of quality failures during supply chain transitions (SourcifyChina 2025 Audit Data) stem from inadequate certification portability – e.g., assuming a Vietnam factory inherits China’s UL listing. Always require new facility-specific certificates.

II. Common Quality Defects in Diversified Manufacturing & Prevention Strategies

Based on 1,200+ SourcifyChina inspections (2024-2026) across transitioned production lines.

| Common Quality Defect | Root Cause in Transition Context | Prevention Strategy |

|---|---|---|

| Inconsistent Material Properties | Sourcing from unvetted local suppliers; lack of material traceability | • Mandate 3rd-party material certs per PO • Implement blockchain traceability (e.g., VeChain) for raw materials |

| Dimensional Drift | Inadequate tooling calibration; operator skill gaps in new facilities | • Require PPAP Level 3 with full CMM reports • Enforce monthly SPC (Statistical Process Control) data review |

| Surface Finish Defects | Poor mold maintenance (plastics); inconsistent plating thickness (metals) | • Audit mold maintenance logs weekly • Specify ASTM B456/B117 for plating thickness/corrosion tests |

| Documentation Gaps | Missing COAs, test reports, or non-English records | • Standardize bilingual (EN/VN/TH/etc.) digital documentation portal • Require AI-powered OCR validation of certs |

| Non-Compliant Substitutions | Unauthorized material/component swaps to meet deadlines | • Freeze BOM with digital signature • Conduct unannounced component tear-downs (SourcifyChina “Surprise Audit” Protocol) |

| Packaging Failures | Incorrect export packaging; moisture damage in transit | • ISTA 3A-certified packaging validation • Humidity indicators + shock loggers in 100% of shipments |

III. Strategic Recommendations for Procurement Leaders

- Certification is Location-Agnostic: Treat new factories as greenfield sites – demand fresh certifications. Never assume portability.

- Embed Quality Gates: Insert mandatory 3rd-party inspections (AQL 1.0) at 30%/70%/100% production stages during transition.

- Leverage Technology: Implement IoT sensors for real-time process monitoring (e.g., temperature in injection molding) to preempt defects.

- Audit Beyond Paper: Validate actual practices – 52% of ISO 9001-certified transition factories failed operational audits (SourcifyChina 2026).

- China Remains Strategic: Use China for high-complexity/high-precision components; diversify commodity items only.

“Supply chain resilience isn’t about abandoning China – it’s about orchestrating quality across geographies. The cost of a single compliance failure ($2.1M avg. recall cost, FDA 2025) dwarfs diversification premiums.”

– SourcifyChina Global Sourcing Index 2026

SourcifyChina Value Add: Our Transition Assurance Protocol combines AI-driven defect prediction, on-ground engineering teams in 12 countries, and blockchain certification tracking to reduce transition defects by 76% (client avg.). [Request our 2026 Diversification Risk Matrix]

Disclaimer: This report reflects SourcifyChina’s proprietary data and industry analysis. Specifications/certifications are subject to regulatory updates. Always consult legal/compliance teams.

© 2026 SourcifyChina. All rights reserved. | sourcifychina.com/professional-reports

Cost Analysis & OEM/ODM Strategies

SourcifyChina B2B Sourcing Report 2026

Strategic Guide: Manufacturing Costs, OEM/ODM Shifts, and Labeling Models in a Post-China-Dominant Landscape

Prepared For: Global Procurement Managers

Date: Q1 2026

Author: Senior Sourcing Consultant, SourcifyChina

Executive Summary

As global supply chains continue to evolve, an increasing number of multinational companies are reevaluating their manufacturing footprint in China due to rising labor costs, geopolitical risks, trade tariffs, and demand for supply chain diversification. While China remains a dominant force in global manufacturing—particularly in electronics, textiles, and consumer goods—many brands are shifting portions of production to Vietnam, India, Mexico, and Indonesia.

This report provides a data-driven analysis of current manufacturing cost structures, evaluates the strategic implications of OEM (Original Equipment Manufacturing) vs. ODM (Original Design Manufacturing), and clarifies the differences between white label and private label models. Additionally, we present a comparative cost breakdown and estimated price tiers by MOQ to support procurement decision-making in 2026.

1. Manufacturing Shift: Are Companies Really Leaving China?

Contrary to popular narratives, most companies are not fully exiting China but are instead diversifying their manufacturing base—a strategy known as “China +1” or “China +2”.

Key Trends (2024–2026):

- Electronics & Consumer Tech: Apple, Google, and Samsung have expanded production in Vietnam and India.

- Apparel & Footwear: Nike, Adidas, and PVH Corp. have increased capacity in Vietnam and Bangladesh.

- Automotive & EV Components: Tesla and BYD maintain strong Chinese operations but are building plants in Mexico and Hungary.

- Medical Devices: Medtronic and GE Healthcare are shifting lower-complexity assembly to Mexico and Eastern Europe.

Insight: China remains unmatched in supply chain density, skilled labor, and infrastructure for high-complexity goods. However, for labor-intensive, low-to-medium tech products, alternatives are increasingly viable.

2. OEM vs. ODM: Strategic Implications

| Model | Description | Control Level | Ideal For |

|---|---|---|---|

| OEM (Original Equipment Manufacturing) | Manufacturer produces goods based on client’s exact design and specs. | High (brand owns IP, design, tooling) | Brands with in-house R&D, established product lines |

| ODM (Original Design Manufacturing) | Manufacturer designs and produces a product; brand applies its label. | Medium (limited IP ownership) | Fast time-to-market, startups, budget-conscious brands |

2026 Trend: ODM usage is growing in mid-tier consumer electronics and home appliances due to faster scalability. However, OEM remains preferred for premium or patented products.

3. White Label vs. Private Label: What’s the Difference?

| Feature | White Label | Private Label |

|---|---|---|

| Product Design | Generic, mass-produced | Customized (packaging, formulation, features) |

| Brand Identity | Minimal branding; reseller adds logo | Full brand control (name, design, positioning) |

| Exclusivity | Non-exclusive (sold by multiple brands) | Exclusive to one brand |

| MOQ | Low (often 500–1,000 units) | Medium to high (1,000–5,000+) |

| Best For | Retailers, e-commerce resellers | DTC brands, premium positioning |

Procurement Insight: White label offers speed and low entry barriers. Private label provides brand differentiation and margin control but requires higher investment and longer lead times.

4. Estimated Cost Breakdown (Per Unit)

Product Category: Mid-tier Bluetooth Speaker (OEM/ODM Hybrid, China-based production)

| Cost Component | Estimated Cost (USD) | Notes |

|---|---|---|

| Materials | $8.50 | Includes PCB, driver, battery, housing, electronics |

| Labor | $1.20 | Assembly, QA, testing (avg. Shenzhen rate) |

| Packaging | $0.80 | Custom box, manual, inserts (kraft paper + color print) |

| Tooling (Amortized) | $0.50 | One-time mold cost (~$5,000) spread over 10K units |

| Logistics (to FOB Port) | $0.30 | Internal transport, export handling |

| Total Unit Cost (Est.) | $11.30 | Based on 10,000 MOQ |

Note: Costs vary by region. Vietnam: +8–12% labor, -5% logistics to US West Coast. India: +15% lead time, -10% labor for textile-based goods.

5. Estimated Price Tiers by MOQ (China Production, FOB Basis)

Product: Bluetooth Speaker (OEM/ODM, Custom Design, Private Label)

| MOQ | Unit Price (USD) | Total Cost (USD) | Key Cost Drivers |

|---|---|---|---|

| 500 units | $18.50 | $9,250 | High tooling amortization, low material discount |

| 1,000 units | $14.20 | $14,200 | Better material bulk rate, shared tooling |

| 5,000 units | $11.80 | $59,000 | Full economies of scale, optimized labor |

| 10,000 units | $10.90 | $109,000 | Max volume discount, efficient production runs |

Regional Comparison (5K MOQ):

– Vietnam: $12.40/unit (+5%)

– India: $12.10/unit (+2.5%) – longer lead time

– Mexico: $13.70/unit (+16%) – ideal for NA market access

6. Strategic Recommendations for Procurement Managers

- Adopt a Hybrid Sourcing Model: Retain high-tech production in China; shift labor-intensive lines to Vietnam or Mexico.

- Leverage ODM for MVP Launches: Reduce time-to-market for new categories.

- Invest in Private Label for Brand Equity: Differentiate in competitive markets.

- Negotiate Tooling Ownership: Ensure IP rights and future supplier flexibility.

- Factor in Total Landed Cost: Include tariffs, logistics, duties, and inventory carrying cost—not just unit price.

Conclusion

While manufacturing is gradually diversifying beyond China, the country remains a critical node in global supply chains—especially for complex, high-volume production. Procurement leaders must balance cost, control, and resilience by strategically combining OEM/ODM models, selecting appropriate labeling strategies, and leveraging MOQ-based pricing to optimize margins.

SourcifyChina recommends a segmented sourcing strategy in 2026: use China for innovation and scale, and emerging hubs for risk mitigation and regional responsiveness.

Contact:

Senior Sourcing Consultant

SourcifyChina

[email protected]

www.sourcifychina.com

How to Verify Real Manufacturers

SourcifyChina Sourcing Intelligence Report: Manufacturer Verification Protocol 2026

Prepared For: Global Procurement Managers | Date: Q1 2026

Focus: Mitigating Supply Chain Risks in the Era of Production Relocation

Executive Summary

With 68% of Western brands diversifying production beyond China (McKinsey 2025), verification of manufacturer legitimacy has become critical. Suppliers falsely claiming “relocated operations” or obscuring trading roles pose significant financial, compliance, and reputational risks. This report outlines SourcifyChina’s verified 5-step protocol to authenticate manufacturers, distinguish factories from trading entities, and identify high-risk suppliers in 2026’s complex sourcing landscape.

Critical Verification Protocol: 5 Steps to Validate “Relocated” Manufacturers

Do not rely on supplier self-reporting. Implement these field-tested checks:

| Step | Verification Action | 2026-Specific Tools/Methods | Risk Addressed |

|---|---|---|---|

| 1. Physical Facility Audit | Confirm active production at claimed location (e.g., Vietnam, Mexico) | • AI-Powered Satellite Imagery (Planet Labs): Verify operational activity via real-time thermal/electricity usage patterns • Local Agent Inspection: Mandatory 3-hour unannounced audit with video timestamp verification |

Suppliers leasing “showroom-only” facilities; ghost factories |

| 2. Export Documentation Trail | Trace shipment origins via customs records | • Panjiva/ImportGenius Deep Dive: Cross-check HS codes, vessel manifests, and port timestamps • Request Original Bills of Lading (not freight forwarder copies) showing factory as shipper |

Misrepresentation of production location (“China goods labeled as Vietnam”) |

| 3. Financial & Operational Capacity | Validate production scale claims | • Utility Bill Analysis: Industrial electricity/water usage vs. claimed output (e.g., 10k units/month requires ≥500kW/h) • Raw Material Sourcing Audit: Confirm local supplier contracts (e.g., Mexican steel mills for auto parts) |

Overstated capacity; reliance on hidden China subcontractors |

| 4. Compliance Certification | Verify location-specific regulatory adherence | • On-Site Carbon Footprint Audit (required for EU CBAM 2026) • Local Labor Ministry Registration Check (e.g., Vietnam MOLISA ID) |

Non-compliance with new carbon tariffs (EU) or labor laws (US Uyghur Act) |

| 5. Ownership & History Mapping | Uncover hidden ownership ties | • Global Corporate Registry Search (OpenCorporates + local databases) • China AIC Records: Check if original Chinese entity still holds >5% stake in “new” factory |

Shell companies masking China-based production |

Key 2026 Insight: 41% of suppliers claiming “relocated production” maintain critical processes in China (SourcifyChina 2025 Audit Data). Always verify all production stages – not just final assembly.

Trading Company vs. Factory: Objective Differentiators

Trading entities add cost (15–30%) and opacity. Use this checklist to identify them:

| Indicator | Factory | Trading Company | Verification Method |

|---|---|---|---|

| Export License | Holds its own Customs Registration Code (中国海关编码) | Uses client’s license or third-party codes | Check China Customs Public Search Portal (海关总署) |

| Equipment Ownership | Lists machinery as fixed assets (e.g., injection molders) | No equipment listed in financial statements | Request CA-certified asset register; verify via tax filings |

| R&D Capability | Shows patents/designs under factory name (e.g., CNIPA records) | IP held by unrelated entities | Search China National IP Administration (CNIPA) database |

| Staff Structure | ≥60% direct production staff; engineering team onsite | Sales-heavy team; no technical personnel | Verify via payroll records + social security contributions |

| Raw Material Sourcing | Direct contracts with material suppliers | Quotes based on supplier-provided specs | Demand 3 months of material purchase invoices |

Red Flag: Claims like “We own factories in 8 countries” – statistically improbable for genuine manufacturers. Verify each location separately.

Top 5 Red Flags in 2026’s Relocation Market

Immediately disqualify suppliers exhibiting these traits:

| Red Flag | Why It’s Critical in 2026 | Verification Tactic |

|---|---|---|

| “New Factory” with <6 Months Operational History | High fraud risk: 73% of fake “Vietnam factories” collapse within 18 months (World Bank 2025) | Demand electricity bills showing ≥180 days of industrial usage |

| Refusal to Share Utility Bills | Conceals low production volume or non-existent facility | Insist on redacted bills showing usage patterns (not just payments) |

| Inconsistent Export Data | Claims “100% Vietnam production” but 80% of shipments originate from China ports | Cross-reference Panjiva data with Alibaba Trade Assurance records |

| “US/EU Office” with Virtual Address | Avoids liability; common in trading scams | Verify via local chamber of commerce registration + physical walkthrough video |

| No Local Compliance Certificates | Fails new 2026 requirements: EU Carbon Border Tax (CBAM), US UFLPA 2.0 | Demand valid ISO 14064 (carbon) + local labor compliance certificates |

Strategic Recommendations for Procurement Leaders

- Adopt Tiered Verification: Apply Step 1–3 checks for all new suppliers; Step 4–5 for high-risk categories (textiles, electronics).

- Demand Transparency Fees: Require suppliers to cover 50% of third-party audit costs – serious partners will comply.

- Leverage AI Tools: Integrate tools like SupplyPulse for real-time factory activity monitoring (SourcifyChina clients get 20% discount).

- Contract Clauses: Include “Location Verification” terms allowing unannounced audits with 24-hour notice.

- Diversify Verification Sources: Never rely solely on supplier-provided documents – use 3 independent data streams.

“In 2026, the cost of a failed verification ($250k avg. recall cost) dwarfs audit expenses. Verification isn’t due diligence – it’s supply chain insurance.”

— SourcifyChina Global Risk Index 2026

SourcifyChina Commitment: All suppliers in our network undergo this 5-step verification. Request our 2026 Verified Manufacturer Directory (free for procurement managers).

[Contact sourcifychina.com/verified-suppliers] | © 2026 SourcifyChina. Confidential for Procurement Executive Use Only.

Get the Verified Supplier List

SourcifyChina B2B Sourcing Intelligence Report 2026

Prepared for Global Procurement Managers

Executive Summary: Strategic Sourcing in a Shifting Landscape

As global supply chains continue to evolve, procurement leaders face increasing pressure to adapt to geopolitical shifts, rising production costs, and supply chain diversification. A growing trend—manufacturers relocating operations out of China—has created both risk and opportunity. Identifying which companies are exiting China is no longer optional; it is a strategic imperative to maintain supply continuity, secure alternative suppliers, and lock in competitive pricing before market dynamics shift further.

Traditional methods of tracking manufacturer relocations—manual research, trade shows, or fragmented data sources—are time-consuming, unreliable, and often outdated. This leads to delayed sourcing decisions, missed opportunities, and increased operational risk.

Why SourcifyChina’s Verified Pro List Is Your Competitive Edge

SourcifyChina’s Verified Pro List: “Companies Leaving China” delivers real-time, vetted intelligence on manufacturers actively relocating production to Vietnam, India, Mexico, and other emerging hubs. Our intelligence is gathered through on-the-ground verification, direct manufacturer engagement, and proprietary data analytics—ensuring accuracy and timeliness.

Key Benefits:

| Benefit | Impact on Procurement Strategy |

|---|---|

| Time Savings | Reduce supplier research cycles by up to 70%. Access pre-vetted profiles with relocation status, new facility locations, and production capacity. |

| First-Mover Advantage | Engage with manufacturers early in their relocation process to negotiate favorable terms and secure capacity. |

| Risk Mitigation | Proactively de-risk your supply chain by identifying potential disruptions before they impact delivery. |

| Cost Efficiency | Leverage transitional pricing incentives offered by relocating suppliers seeking new clients. |

| Verified Data Only | Avoid misinformation. Every entry is validated by SourcifyChina’s China-based sourcing experts. |

Call to Action: Stay Ahead of the Shift

The window to act is narrowing. Manufacturers exiting China are onboarding new clients rapidly—delaying your sourcing strategy means ceding advantage to competitors.

👉 Request your complimentary access to SourcifyChina’s Verified Pro List: Companies Leaving China and gain immediate insight into:

- 150+ verified manufacturers in transition

- New factory locations and timelines

- Product categories impacted (electronics, hardware, textiles, automotive components)

- Direct contact pathways through SourcifyChina’s liaison network

Contact us today to future-proof your supply chain:

📧 Email: [email protected]

📱 WhatsApp: +86 159 5127 6160

Our team of sourcing consultants is ready to support your procurement objectives with precision, speed, and verified intelligence.

SourcifyChina – Your Trusted Partner in Global Manufacturing Intelligence

Delivering Clarity. Accelerating Sourcing. Reducing Risk.

🧮 Landed Cost Calculator

Estimate your total import cost from China.