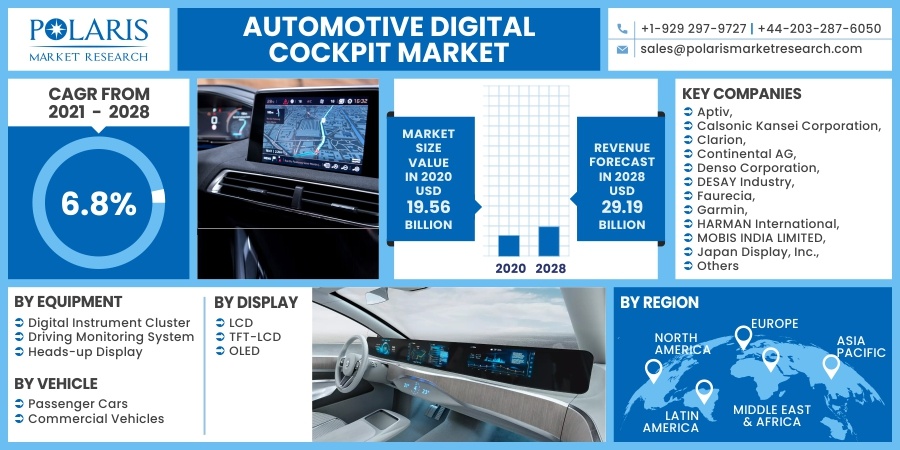

The global automotive instrument cluster market is experiencing robust growth, driven by increasing demand for advanced driver information systems, digital displays, and enhanced vehicle safety features. According to Mordor Intelligence, the market was valued at USD 10.8 billion in 2023 and is projected to reach USD 16.2 billion by 2029, growing at a CAGR of approximately 6.8% during the forecast period. This expansion is fueled by the rising adoption of digital and reconfigurable instrument clusters in both electric and internal combustion engine vehicles, alongside growing consumer preference for connected and intuitive cockpit experiences. As automotive OEMs prioritize digitalization and human-machine interface (HMI) innovation, leading manufacturers are investing heavily in next-generation cluster technologies. In this evolving landscape, nine key players have emerged as dominant forces, shaping the future of in-vehicle instrumentation through advancements in display resolution, software integration, and functional safety standards.

Top 9 Car Instrument Cluster Manufacturers 2026

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Car Instrument Cluster

H2: 2026 Market Trends for Car Instrument Clusters – A Convergence of Digitization, Integration, and Experience

The car instrument cluster market in 2026 is poised for significant transformation, driven by the accelerating shift towards electrification, autonomy, connectivity, and heightened consumer demand for immersive digital experiences. The traditional cluster is rapidly evolving into a central component of the vehicle’s digital cockpit ecosystem. Here are the key trends shaping the market in 2026:

-

Dominance of Full Digital Clusters (TFT & OLED):

- Market Shift: By 2026, full digital instrument clusters (replacing analog dials with high-resolution TFT or OLED displays) will transition from a premium feature to a mainstream expectation, even in mid-tier segments. OLED adoption will grow significantly due to superior contrast, flexibility, and energy efficiency (crucial for EVs).

- Driver: Demand for customization, dynamic content presentation (navigation, ADAS alerts, entertainment), and seamless integration with larger infotainment screens.

-

Rise of the “Cockpit Domain Controller” (CDC) Architecture:

- Consolidation: The trend towards centralized electronic/electrical (E/E) architectures will accelerate. Instead of separate ECUs for cluster, infotainment, and ADAS, a powerful Cockpit Domain Controller will handle multiple functions on a single high-performance chip (e.g., Qualcomm Snapdragon Automotive, NVIDIA DRIVE).

- Impact: Enables seamless content sharing between cluster and center stack (extended displays, video streaming), faster software updates (OTA), reduced wiring complexity, lower cost, and improved performance. The cluster becomes a key output of the CDC, not an isolated system.

-

Integration with Advanced Driver Assistance Systems (ADAS) & Automation:

- Critical Interface: As Level 2+ and Level 3 systems become more common, the cluster becomes the primary interface for conveying system status (engaged, limited, disengaged), driver monitoring system (DMS) alerts, and takeover requests.

- Visualization: Sophisticated 3D graphics, augmented reality (AR) overlays (e.g., projecting navigation arrows onto a camera view of the road within the cluster), and predictive driving information will be displayed, enhancing situational awareness and trust in automation.

-

Enhanced Personalization and User Experience (UX):

- Customization: Drivers will expect deep personalization – customizable layouts, themes, preferred information priorities (e.g., range vs. speed), and integration with personal profiles synced via cloud or smartphone.

- Ambient Integration: Clusters will integrate with ambient lighting and sound systems, dynamically changing visuals and cues based on driving mode (Eco, Sport, Comfort), navigation turn-by-turn, or incoming alerts, creating a holistic sensory experience.

-

Expansion of Display Size and Form Factor Innovation:

- Larger & Wider: Display sizes will continue to grow, with panoramic displays spanning the dashboard (integrating cluster and center stack) becoming more prevalent, especially in premium and EV segments.

- Curved & Freeform: OLED technology enables curved and freeform displays that conform better to the driver’s line of sight, improving ergonomics and aesthetics.

- Augmented Reality (AR) HUD Synergy: While not the cluster itself, the cluster will work in concert with AR-HUDs, providing complementary information. The cluster may handle complex data, while the HUD projects critical navigation and ADAS cues onto the windshield.

-

Focus on Safety and Driver Attention Management:

- Glance Optimization: Design will prioritize minimizing driver distraction. Information will be presented intuitively, with critical data (speed, warnings) in the primary line of sight. Animations will be subtle.

- DMS Integration: Tight integration with DMS (using cabin cameras) will allow the cluster to display alerts for drowsiness, inattention, or distraction, potentially adjusting information density or issuing warnings.

-

Software-Defined Vehicles (SDV) and Over-the-Air (OTA) Updates:

- Dynamic Evolution: The cluster’s functionality and appearance will no longer be fixed at purchase. OEMs will use OTA updates to push new features, UI/UX improvements, bug fixes, and even entirely new cluster themes or capabilities post-purchase, extending the vehicle’s lifecycle and creating recurring revenue potential.

- Cybersecurity: As a connected software platform, robust cybersecurity measures for the cluster and its communication with the CDC will be paramount.

-

Sustainability and Efficiency (Especially for EVs):

- Energy Optimization: OLED displays and efficient software will be crucial for maximizing EV range. Clusters will feature optimized brightness, dynamic refresh rates, and “sleep” modes.

- Material Use: Increased focus on sustainable materials within the cluster housing and components.

Conclusion for 2026:

The car instrument cluster in 2026 will be far more than just a speedometer and tachometer. It will be a dynamic, intelligent, and personalized hub within the centralized digital cockpit. Driven by electrification, automation, and the software-defined vehicle paradigm, the market will be dominated by large, high-resolution digital displays (TFT/OLED) powered by Cockpit Domain Controllers. Success will hinge on seamless integration with ADAS, delivering exceptional UX through personalization and safety-focused design, and enabling continuous evolution via OTA updates. The cluster’s role will be central to building driver trust in automation and creating a compelling overall in-vehicle experience.

Common Pitfalls Sourcing Car Instrument Clusters (Quality, IP)

Sourcing car instrument clusters—especially from third-party or overseas suppliers—exposes manufacturers and aftermarket businesses to significant risks related to both quality and intellectual property (IP). Failing to address these pitfalls can lead to costly recalls, legal disputes, and reputational damage.

Quality-Related Pitfalls

1. Inconsistent Manufacturing Standards

Suppliers, particularly in regions with less stringent regulatory oversight, may not adhere to automotive-grade quality standards (e.g., ISO/TS 16949 or IATF 16949). This can result in clusters with poor durability, inaccurate readings, or premature failure under real-world conditions.

2. Use of Substandard Components

To reduce costs, some suppliers substitute genuine or high-reliability components (e.g., LCD/LED displays, microcontrollers, sensors) with inferior alternatives. This compromises long-term performance and safety, especially in extreme temperatures or high-vibration environments.

3. Lack of Environmental and Reliability Testing

Reputable clusters undergo rigorous testing for temperature extremes, humidity, vibration, and electromagnetic interference (EMI). Many third-party suppliers skip or inadequately perform these tests, leading to field failures and safety hazards.

4. Poor Calibration and Software Integration

Instrument clusters must be precisely calibrated and integrated with vehicle ECUs. Poorly sourced clusters often have software incompatibilities, incorrect speedometer or tachometer readings, or fail to communicate with other systems (e.g., ABS, airbag warnings).

5. Inadequate Quality Control and Traceability

Many suppliers lack robust QC processes or batch traceability. Without proper documentation or testing records, identifying the root cause of failures or executing recalls becomes extremely difficult.

Intellectual Property (IP)-Related Pitfalls

1. Risk of Counterfeit or Reverse-Engineered Products

Some suppliers offer clusters that mimic OEM designs but are reverse-engineered without licensing. These products infringe on design patents, trademarks, and software copyrights, exposing buyers to legal liability.

2. Unauthorized Use of Proprietary Software and Firmware

OEM clusters contain proprietary firmware that controls communication protocols (e.g., CAN bus), display logic, and diagnostic functions. Sourcing clusters with unauthorized firmware copies can violate software licensing agreements and expose the buyer to intellectual property lawsuits.

3. Lack of IP Warranty and Indemnification

Many low-cost suppliers do not provide IP warranties or indemnification against infringement claims. If a legal dispute arises, the buyer—not the supplier—may be held responsible for damages or legal costs.

4. Gray Market and Unauthorized Distribution

Clusters sourced through unofficial channels may be stolen, diverted, or produced beyond authorized volumes. These units often lack proper IP clearance and may violate distribution agreements between OEMs and their partners.

5. Difficulties in Regulatory Compliance and Homologation

Using non-OEM or unapproved clusters can lead to non-compliance with regional automotive regulations (e.g., ECE, DOT, FMVSS). This not only affects vehicle certification but may also constitute IP misuse if approved designs are duplicated without authorization.

Mitigation Strategies

To avoid these pitfalls, buyers should:

– Conduct thorough supplier audits and request quality certifications.

– Require sample testing under real-world conditions.

– Verify IP legitimacy through legal diligence and supplier warranties.

– Source from authorized distributors or OEM-approved partners.

– Include strong IP indemnification clauses in procurement contracts.

Ignoring these aspects during sourcing can result in compromised vehicle safety, regulatory non-compliance, and exposure to costly litigation.

Logistics & Compliance Guide for Car Instrument Cluster

Overview

The car instrument cluster is a critical component in vehicle manufacturing and after-sales service, responsible for displaying essential driving information such as speed, fuel level, engine RPM, and warning indicators. Due to its electronic nature, safety implications, and regulatory requirements, specific logistics and compliance protocols must be followed throughout its supply chain journey.

Regulatory Compliance

Automotive Safety Standards (ISO 26262)

The instrument cluster must comply with ISO 26262, the international standard for functional safety in road vehicles. This includes:

– Adherence to Automotive Safety Integrity Level (ASIL) requirements.

– Implementation of safety mechanisms to prevent display failures or incorrect readings.

– Documentation of safety analyses (e.g., FMEA, FTA) throughout design and production.

Electromagnetic Compatibility (EMC)

Instrument clusters must meet EMC regulations (e.g., CISPR 25, ISO 11452) to ensure they do not emit or are not susceptible to electromagnetic interference that could affect other vehicle systems.

Environmental Regulations

- RoHS (Restriction of Hazardous Substances): Compliance required for all electronic components; restricts substances like lead, mercury, and cadmium.

- REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals): Applies to materials used in manufacturing; requires disclosure of SVHCs (Substances of Very High Concern).

- ELV (End-of-Life Vehicles Directive): Mandates recyclability and restricts the use of certain hazardous materials.

Regional Certification Requirements

- Europe: CE marking, ECE R121 (for malfunction indication), and type-approval under EU Framework Regulation (EU) 2018/858.

- United States: Compliance with FMVSS No. 101 (controls and displays) and EPA regulations for materials.

- China: CCC (China Compulsory Certification) and GB standards.

- Other Markets: INMETRO (Brazil), KC Mark (Korea), PSE (Japan).

Packaging & Handling

Packaging Specifications

- Use static-dissipative or anti-static packaging to protect sensitive electronic components.

- Include protective foam inserts to prevent mechanical shock and vibration damage.

- Seal packaging in moisture-barrier bags with desiccants if shipping to humid environments.

- Label packages with “Fragile,” “Electrostatic Sensitive,” and orientation indicators.

Handling Procedures

- Train warehouse and logistics personnel on ESD (Electrostatic Discharge) protection protocols.

- Use grounded workstations and wrist straps during handling.

- Avoid exposure to extreme temperatures, moisture, and direct sunlight.

- Minimize stacking height to prevent crushing damage.

Transportation & Logistics

Mode of Transport

- Air Freight: Preferred for time-sensitive deliveries; must comply with IATA Dangerous Goods Regulations if batteries are attached.

- Ocean Freight: Cost-effective for bulk shipments; requires moisture and salt-air protection.

- Road Transport: Common for regional distribution; ensure climate-controlled or dry vans are used.

Temperature & Environmental Controls

- Maintain storage and transport temperatures between 0°C and 40°C unless otherwise specified.

- Monitor humidity levels to prevent condensation (ideally <60% RH).

- Use data loggers to record temperature and humidity during transit.

Customs Documentation

- Prepare accurate commercial invoices, packing lists, and certificates of origin.

- Include compliance documentation (e.g., RoHS, REACH, ISO 26262 reports, test certificates).

- Classify under correct HS Code (e.g., 9029.20 for speedometers and tachometers).

Inventory & Warehouse Management

Storage Conditions

- Store in clean, dry, temperature-controlled environments.

- Keep away from sources of EMI (e.g., motors, transformers).

- Implement FIFO (First In, First Out) to prevent component aging.

Traceability

- Use barcode or RFID tagging to track individual units.

- Maintain traceability records for at least 10–15 years (as per automotive industry standards).

- Record batch numbers, production dates, and software/firmware versions.

After-Sales & Reverse Logistics

Warranty & Repair Handling

- Establish authorized service centers with trained technicians.

- Use tamper-evident seals to identify unauthorized repairs.

- Return defective units with failure analysis reports.

End-of-Life & Recycling

- Follow ELV Directive and local e-waste regulations for disposal.

- Partner with certified e-waste recyclers.

- Recover and recycle materials such as plastics, metals, and circuit boards.

Conclusion

Transporting and managing car instrument clusters requires strict adherence to global compliance standards, careful handling, and detailed logistics planning. By following this guide, manufacturers and logistics providers can ensure product integrity, regulatory compliance, and customer safety throughout the product lifecycle.

Conclusion for Sourcing a Car Instrument Cluster:

Sourcing a car instrument cluster requires careful consideration of several key factors including compatibility, quality, cost, and supplier reliability. Whether sourcing new, aftermarket, or used units, it is essential to ensure the cluster matches the vehicle’s make, model, year, and trim level to guarantee proper fitment and functionality. Technological advancements, such as digital dashboards and integrated driver assistance systems, further emphasize the need for precise specifications and software compatibility during the sourcing process.

Purchasing from reputable suppliers or OEM manufacturers ensures reliability and reduces the risk of malfunctions, while cost-effective aftermarket options may be viable with thorough vetting. Additionally, considerations such as warranty coverage, return policies, and technical support play a crucial role in minimizing downtime and repair costs.

In conclusion, a strategic and well-informed approach to sourcing car instrument clusters—balancing quality, compatibility, and cost—ensures optimal vehicle performance, customer satisfaction, and long-term reliability. Establishing strong relationships with trusted suppliers and staying updated on automotive technology trends will further enhance sourcing effectiveness in an evolving automotive landscape.