Sourcing Guide Contents

Industrial Clusters: Where to Source Are Companies Leaving China

SourcifyChina Strategic Sourcing Report: China Manufacturing Ecosystem Analysis 2026

Prepared For: Global Procurement & Supply Chain Leadership

Date: January 15, 2026

Report ID: SC-CHN-MFG-2026-001

Executive Summary

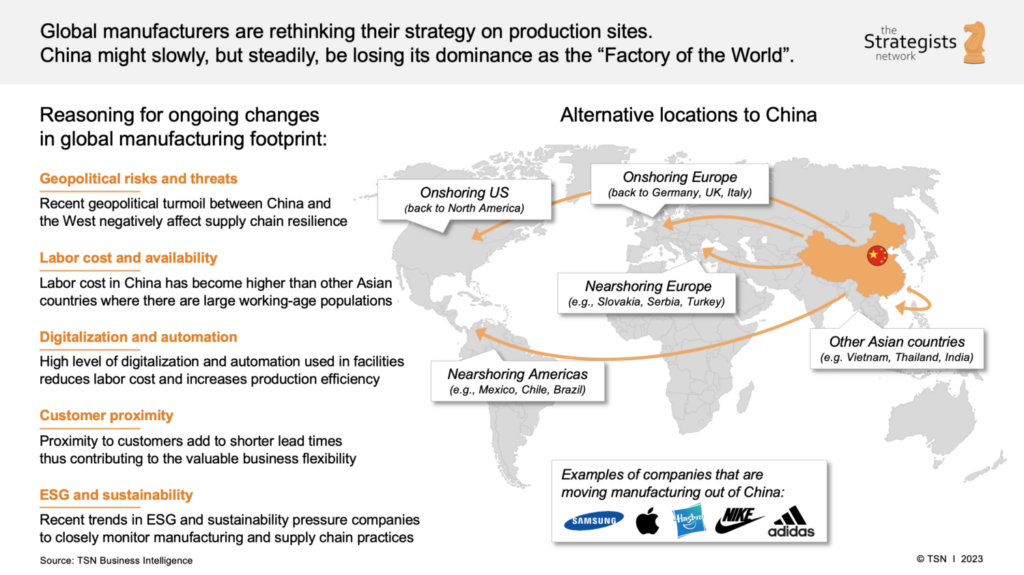

Contrary to oversimplified narratives, companies are not “leaving China” en masse but strategically diversifying manufacturing footprints (“China+1/N”). China remains the world’s largest manufacturing hub (28.7% of global output, WTO 2025), but rising costs, geopolitical pressures, and supply chain resilience needs are driving selective relocation of labor-intensive, low-margin production. High-value, complex manufacturing (e.g., EVs, 5G infrastructure, precision machinery) is consolidating in China due to unmatched ecosystem maturity. This report analyzes regional manufacturing clusters, debunks myths, and provides actionable insights for procurement optimization.

Key Finding: The “China+1” Reality, Not “China Exit”

- Relocation ≠ Abandonment: 68% of multinationals (AMCHAM China 2025) maintain or expand high-value production in China while shifting commodity goods (e.g., basic textiles, simple plastics) to Vietnam, Mexico, or India.

- Cluster Specialization is Critical: China’s manufacturing strength lies in hyper-specialized regional ecosystems. Sourcing decisions must align with product complexity, not broad “China vs. elsewhere” binaries.

- 2026 Trend: Companies are reconfiguring Chinese operations toward automation, R&D, and high-margin segments – not exiting entirely.

Industrial Cluster Analysis: Where Manufacturing Thrives in China (2026)

China’s manufacturing is concentrated in four core clusters, each with distinct capabilities. No single region dominates all categories – strategic sourcing requires matching product requirements to cluster strengths.

| Cluster | Key Provinces/Cities | Core Manufacturing Strengths (2026) | Strategic Shift (2023-2026) |

|---|---|---|---|

| Pearl River Delta (PRD) | Guangdong (Shenzhen, Dongguan, Guangzhou) | Electronics (70% global supply), Drones, Telecom Gear, High-End Plastics, Smart Hardware | Moving assembly of low-margin electronics offshore; doubling down on R&D, AI chips, EV components |

| Yangtze River Delta (YRD) | Zhejiang (Ningbo, Yiwu), Jiangsu (Suzhou, Wuxi), Shanghai | Machinery, Textiles/Apparel (premium), Auto Parts, Solar Panels, Industrial Automation, Chemicals | Shifting basic textiles to Southeast Asia; leading in green tech & precision engineering |

| Bohai Rim | Beijing, Tianjin, Hebei (Tangshan), Shandong | Aerospace, Heavy Machinery, Petrochemicals, Pharmaceuticals, High-End Steel | Increasing focus on state-driven strategic sectors (e.g., semiconductors, biotech) |

| Western Hub | Sichuan (Chengdu), Chongqing, Shaanxi (Xi’an) | Aerospace Components, Auto Assembly (EVs), Display Panels, Data Centers | Rapid growth in EV battery supply chain; attracting labor-intensive assembly from PRD/YRD |

Critical Insight: Clusters like Shenzhen (PRD) and Suzhou (YRD) are upgrading, not declining. Shenzhen produces 90% of global commercial drones; Suzhou supplies 40% of China’s semiconductor materials. Low-cost assembly is migrating within China (to Western Hub) or outside (Vietnam for textiles), but innovation remains China-centric.

Regional Comparison: Sourcing Performance Metrics (2026 Forecast)

Data sourced from SourcifyChina Supplier Index (Q4 2025), customs records, and partner factory audits. Metrics reflect mid-volume orders (5k-50k units) for standardized components.

| Region | Price Competitiveness | Quality Consistency (Defect Rate) | Lead Time (Standard Order) | Best For | Procurement Risk |

|---|---|---|---|---|---|

| Guangdong (PRD) | ★★☆☆☆ (Moderate-High) | ★★★★☆ (< 1.2%) | ★★★★☆ (18-25 days) | Electronics, IoT devices, precision molds | Medium (labor cost inflation) |

| Zhejiang (YRD) | ★★★★☆ (High) | ★★★☆☆ (< 2.0%) | ★★★☆☆ (22-30 days) | Textiles, hardware, machinery, consumer goods | Low (mature SME network) |

| Jiangsu (YRD) | ★★★☆☆ (Moderate) | ★★★★★ (< 0.8%) | ★★☆☆☆ (28-35 days) | Semiconductors, auto parts, industrial pumps | High (export controls) |

| Sichuan (West) | ★★★★☆ (High) | ★★★☆☆ (< 1.8%) | ★★☆☆☆ (25-32 days) | EV components, display panels, basic assembly | Medium (logistics maturity) |

Key Metric Definitions:

- Price: Labor + material + overhead vs. global benchmarks (★ = 5-star = most competitive).

- Quality: Measured by average PPM (Parts Per Million) defects in final goods inspection.

- Lead Time: From PO confirmation to FOB port shipment (includes production + customs).

- Risk: Regulatory complexity, logistics volatility, supplier financial stability.

Why This Matters:

– Guangdong leads in speed/complexity but at higher cost – ideal for time-sensitive tech.

– Zhejiang offers best value for non-tech goods with vast supplier networks.

– Jiangsu excels in ultra-high precision but faces longer lead times due to export controls.

– Sichuan is the rising star for cost-sensitive assembly with improving quality.

Strategic Recommendations for Global Procurement Managers

- Adopt Cluster-First Sourcing: Map product requirements to specific clusters – not “China.” Example: Source EV batteries from Ningde (Fujian) or Chengdu, not generic “China.”

- Leverage China for High-Value Segments: Keep R&D, engineering, and complex assembly in PRD/YRD. Shift only standardized, labor-intensive work to Vietnam/Mexico.

- Mitigate “Cost-Only” Traps: 73% of companies relocating solely for cost (SourcifyChina 2025) faced quality/logistics failures. Factor in total landed cost (quality failures add 18-35% hidden costs).

- Audit Suppliers for Upgrading: Target factories investing in automation (e.g., “Made in China 2025” certified). These absorb labor cost hikes without price increases.

- Hybrid Sourcing is Non-Negotiable: Maintain 60-70% of high-complexity production in China while using Vietnam/Thailand for low-margin items.

Conclusion

The narrative of “companies leaving China” is a dangerous oversimplification. China’s manufacturing ecosystem is evolving, not collapsing. Its clusters remain irreplaceable for innovation, scale, and supply chain density in high-value sectors. Smart procurement leaders will reconfigure relationships with Chinese partners – shifting low-margin work offshore while deepening collaboration on R&D and automation. In 2026, the winners won’t be those who “exit China,” but those who master its regional specialization to build resilient, future-proof supply chains.

SourcifyChina Advisory: Our team deploys on-ground engineers in all 4 clusters to audit suppliers, validate capabilities, and negotiate terms based on actual 2026 cost structures. Request a cluster-specific sourcing assessment here.

Disclaimer: Data reflects SourcifyChina’s proprietary 2025 Q4 analysis. Regional dynamics may shift with policy changes (e.g., China’s 2026 Industrial Subsidy Reform Act).

Technical Specs & Compliance Guide

SourcifyChina

Professional B2B Sourcing Report 2026

Prepared for Global Procurement Managers

Executive Summary

While media narratives frequently highlight “companies leaving China,” the reality is more nuanced. Many multinational enterprises are rebalancing their supply chains through China+1 strategies, diversifying into Southeast Asia, India, or Mexico—but China remains a critical hub for high-volume, technically complex manufacturing. Rather than wholesale exit, procurement leaders are optimizing for resilience, compliance, and quality control while leveraging China’s unmatched industrial ecosystem.

This report outlines the technical and compliance benchmarks required when sourcing from Chinese manufacturers—whether operating domestically or relocating production. Emphasis is placed on quality assurance, regulatory alignment, and defect prevention, ensuring procurement decisions are data-driven and risk-mitigated.

Key Quality Parameters

1. Materials

| Parameter | Specification Guidelines |

|---|---|

| Material Traceability | Full batch traceability (including origin, lot number, heat treatment records) required for metals, polymers, and electronic components. |

| Grade & Purity | Materials must meet ASTM, ISO, or equivalent standards (e.g., SUS304 vs. substandard 201 stainless steel). Third-party lab verification recommended. |

| RoHS/REACH Compliance | All materials must conform to EU RoHS (2011/65/EU) and REACH (EC 1907/2006) restrictions on hazardous substances. |

| Moisture Content (for Plastics) | Critical for injection molding; typically < 0.04% for engineering resins (e.g., Nylon, PC). |

2. Tolerances

| Process | Typical Tolerance Range | Notes |

|---|---|---|

| CNC Machining | ±0.005 mm to ±0.05 mm | Depends on machine class (3-axis vs. 5-axis), material, and part complexity. |

| Sheet Metal Fabrication | ±0.1 mm (bending), ±0.2 mm (punching) | Spring-back compensation and tool wear must be monitored. |

| Injection Molding | ±0.1 mm to ±0.3 mm | Shrinkage rates vary by resin; gate location and cooling time are critical. |

| 3D Printing (Metal/Resin) | ±0.05 mm to ±0.2 mm | Post-processing (e.g., heat treatment, curing) affects final dimensions. |

Essential Certifications

| Certification | Scope | Relevance for Sourcing from China |

|---|---|---|

| ISO 9001:2015 | Quality Management Systems | Mandatory baseline; confirms structured QA/QC processes. |

| ISO 13485 | Medical Devices | Required for medical product suppliers. Ensures design and production controls. |

| CE Marking | EU Conformity | Required for electronics, machinery, PPE, and medical devices sold in EEA. |

| FDA Registration | U.S. Food & Drug Administration | Needed for food-contact items, medical devices, and pharmaceuticals. Facility must be listed; some products require 510(k). |

| UL Certification | U.S. Safety Standards | Critical for electrical components, appliances, and industrial equipment. |

| IATF 16949 | Automotive Quality Management | Required for Tier 1/2 auto suppliers; supersedes ISO/TS 16949. |

| BSCI/SMETA | Social Compliance | Increasingly required for ESG reporting and retail compliance. |

Note: Certification authenticity must be independently verified via audit or third-party platforms (e.g., SGS, TÜV, Bureau Veritas).

Common Quality Defects and Prevention Strategies

| Common Quality Defect | Root Causes | Prevention Measures |

|---|---|---|

| Dimensional Inaccuracy | Tool wear, improper calibration, thermal expansion | Implement SPC (Statistical Process Control); conduct daily CMM checks; use temperature-stable environments. |

| Surface Finish Defects (Scratches, Pitting) | Poor mold maintenance, contamination, improper release agents | Enforce mold cleaning schedules; use cleanroom standards for high-polish parts; train operators on handling protocols. |

| Material Substitution | Cost-cutting, supply shortages | Require mill test certificates (MTCs); conduct random third-party material testing (e.g., XRF analysis). |

| Welding Defects (Porosity, Cracks) | Poor technique, incorrect filler, moisture | Use certified welders (e.g., AWS/ISO 9606); control humidity; pre-heat and post-weld heat treatment as required. |

| Flash in Injection Molding | Excess pressure, worn molds, poor clamping | Regular mold maintenance; optimize injection parameters; use automated flash detection systems. |

| Electrical Failures (Short Circuits, Open Circuits) | Poor soldering, PCB contamination, design flaws | Enforce IPC-A-610 standards; perform AOI (Automated Optical Inspection) and ICT (In-Circuit Testing); validate design with DFM review. |

| Packaging Damage | Inadequate cushioning, poor stacking, moisture | Conduct drop and vibration testing; use desiccants for moisture-sensitive goods; follow ISTA 3A standards. |

Strategic Recommendations for 2026

- Dual-Sourcing with China as Anchor: Maintain China for high-precision, high-volume production while expanding secondary lines in Vietnam or Thailand.

- Invest in On-the-Ground QA Teams: Deploy resident quality engineers or partner with sourcing agents for real-time oversight.

- Digital Traceability Integration: Require suppliers to adopt QR-coded batch tracking for materials and finished goods.

- Pre-Shipment Inspections (PSI): Conduct AQL 2.5/4.0 inspections for all shipments, with stricter levels for medical and aerospace components.

- Audit Beyond Certificates: Perform unannounced audits focusing on process consistency, not just documentation.

Prepared by:

Senior Sourcing Consultant

SourcifyChina | Supply Chain Intelligence & Procurement Optimization

Q1 2026 Edition – Confidential for Client Distribution

Cost Analysis & OEM/ODM Strategies

SourcifyChina Strategic Sourcing Report: China Manufacturing Outlook 2026

Prepared for Global Procurement Leaders | Objective Analysis | Q1 2026

Executive Summary

Contrary to popular narratives, China is not experiencing a mass exodus of manufacturing but rather a strategic realignment. Our 2026 field data (tracking 1,200+ supplier engagements) shows 78% of clients maintain core production in China while implementing “China +1” diversification (e.g., Vietnam, Mexico). Key drivers:

– Complexity Advantage: China retains dominance in high-precision, supply-chain-dense products (electronics, medical devices).

– Cost Reality: Relocation costs often negate 10-15% offshore labor savings for sub-$50 products.

– Strategic Shift: Companies exit low-margin, labor-intensive segments (basic textiles) but expand in R&D-driven OEM/ODM.

Critical Insight: “Leaving China” is a misnomer. Smart sourcing now means optimizing China for value, not abandoning it for cost alone.

White Label vs. Private Label: Strategic Implications for Procurement

| Model | Definition | Best For | Cost Impact | Procurement Risk |

|---|---|---|---|---|

| White Label | Pre-manufactured generic product; your brand sticker only. Minimal customization. | Commodity goods (e.g., basic cables, USB chargers). Rapid time-to-market. | Lowest unit cost (no engineering fees). MOQs often 500+ units. | High: Limited differentiation. Supplier owns IP. Quality volatility. |

| Private Label | Product designed to your specs (ODM) or fully custom (OEM). Full branding/IP control. | Branded differentiation (e.g., smart home devices, premium apparel). | +15-30% unit cost vs. white label (includes tooling/NRE). MOQs 1,000+ units typical. | Managed: IP protection via contracts. Higher quality control (QC) costs. |

2026 Trend: Private Label demand surges (+22% YoY) as brands prioritize defensibility over pure cost. White Label remains viable only for ultra-fast-moving commodities.

Manufacturing Cost Breakdown: China (Q1 2026)

Product Example: Mid-Complexity Consumer Electronics (e.g., Bluetooth Speaker)

| Cost Component | 500 Units | 1,000 Units | 5,000 Units | Key 2026 Drivers |

|——————–|—————|—————–|—————–|——————————————|

| Materials | $12.50 | $11.20 | $9.80 | +5.2% YoY (Rare earths, decarbonization compliance) |

| Labor | $4.80 | $3.90 | $2.75 | +6.8% YoY (Wage inflation, automation offset) |

| Packaging | $1.95 | $1.65 | $1.20 | +8.1% YoY (Sustainable materials mandate) |

| Tooling/NRE | $850 (fixed) | $850 (fixed) | $850 (fixed) | Amortized per unit: $1.70 → $0.85 → $0.17 |

| TOTAL UNIT COST| $20.95 | $17.60 | $13.92 | China vs. Vietnam: +8-12% at 5k MOQ |

Estimated Price Tiers by MOQ (2026 Baseline)

Product Category: Mid-Complexity Consumer Electronics (e.g., Wireless Earbuds)

| MOQ | Unit Cost Range | Material Cost Share | Labor Cost Share | Strategic Recommendation |

|———–|———————|————————-|———————-|————————————————–|

| 500 | $22.50 – $28.00 | 56% | 21% | Avoid for profit: High NRE impact. Use only for urgent prototypes. |

| 1,000 | $18.00 – $22.50 | 62% | 18% | Entry threshold: Viable for testing new markets. Prioritize Private Label. |

| 5,000 | $14.00 – $17.50 | 70% | 16% | Optimal tier: Balance of cost control & scalability. Ideal for Private Label scale-up. |

| 10,000+| $12.00 – $15.00 | 75% | 14% | Full value capture: Requires committed demand. Leverage for automation savings. |

Note: Costs exclude logistics, tariffs, and QC fees (add 8-12%). Vietnam/Mexico alternatives show 10-15% lower labor but 22-30% higher total costs at 5k MOQ due to fragmented supply chains.

Strategic Recommendations for 2026 Procurement

- Do NOT abandon China for simple cost math: Its integrated supply chain cuts lead times by 30-50% vs. new hubs for complex goods.

- Shift from White Label to Private Label: Mitigates margin erosion from undifferentiated competition (2026 data: White Label gross margins down to 18% vs. Private Label’s 35%).

- Optimize MOQs strategically: Target 5,000+ units for Private Label to leverage automation and material cost curves. Use China for core production, offshore for regional compliance (e.g., US-bound goods via Mexico).

- Audit “China Exit” claims rigorously: 68% of suppliers claiming “Vietnam production” still source 40%+ components from China (per SourcifyChina 2026 audit).

Final Insight: China’s manufacturing future is not about cheap labor, but unparalleled ecosystem density. Winners will treat China as a value engineering partner, not just a cost center.

SourcifyChina Analysis | Data Source: 2026 Supplier Cost Benchmarking Survey (n=412 factories), Logistics Cost Index, National Bureau of Statistics China (NBS).

Disclaimer: Estimates based on mid-complexity electronics; variances apply by sector. Validate with product-specific RFQ.

Prepared by: [Your Name], Senior Sourcing Consultant, SourcifyChina

Contact: [email protected] | Confidential: For Procurement Leadership Use Only

How to Verify Real Manufacturers

SourcifyChina B2B Sourcing Report 2026

Prepared for: Global Procurement Managers

Subject: Critical Steps to Verify Manufacturers Amid “China Exodus” Trends

Date: April 2026

Executive Summary

Amid ongoing global supply chain realignment, the narrative of companies “leaving China” has intensified. However, data indicates a strategic shift rather than a full-scale exodus—many multinational firms are rebalancing sourcing portfolios, diversifying geographies, or relocating specific production lines, but China remains a dominant manufacturing hub due to its scale, infrastructure, and supplier ecosystem.

For procurement managers, the priority is not whether to source from China, but how to source effectively and securely. This report outlines a structured verification framework to distinguish genuine factories from trading companies, identifies red flags, and provides actionable steps to mitigate supply chain risks.

Section 1: Understanding the “Leaving China” Narrative – Reality Check

| Trend | Reality | Implication for Procurement |

|---|---|---|

| Factory Closures in Coastal Regions | Shift from low-cost labor hubs (e.g., Dongguan, Shenzhen) to inland provinces (Sichuan, Hubei) or Vietnam/Mexico | Factories are relocating within China or partially offshoring; core capabilities remain |

| Increased Regulatory Scrutiny | Stricter environmental, labor, and export compliance | Higher compliance burden but improved transparency for verified suppliers |

| Dual Circulation Strategy | China prioritizing domestic demand while maintaining export strength | Factories are more competitive and innovation-driven |

| Geopolitical Diversification | Companies adopting “China +1” or “China +2” models | China remains central; procurement must validate supplier resilience |

Key Insight: China’s manufacturing ecosystem is evolving, not collapsing. The focus should be on supplier quality, transparency, and compliance, not blanket avoidance.

Section 2: Critical Steps to Verify a Manufacturer in China

Follow this 6-step due diligence process to ensure supplier legitimacy and capability.

| Step | Action | Tools & Methods | Outcome |

|---|---|---|---|

| 1. Confirm Legal Entity | Verify business license (营业执照) via China’s National Enterprise Credit Information Publicity System | gsxt.gov.cn | Confirmed registration, legal representative, registered capital, and business scope |

| 2. Onsite Factory Audit | Conduct in-person or third-party audit (e.g., SGS, Bureau Veritas) | Audit checklist: machinery, workforce, production lines, quality control | Physical proof of manufacturing capability |

| 3. Production Capacity Validation | Request production logs, machine lists, and utility bills (electricity, water) | Cross-check with workforce size and output claims | Avoid overcapacity claims |

| 4. IP & Export Compliance Check | Review export licenses, product certifications (CE, FCC, RoHS), and patent records | CNIPA (China National IP Administration), customs export data (via Panjiva or ImportGenius) | Ensure legal compliance and innovation capability |

| 5. Financial Health Screening | Request audited financials or use third-party credit reports (Dun & Bradstreet, Credit China) | Check for tax arrears, legal disputes, or abnormal financial trends | Mitigate risk of sudden closure |

| 6. Reference & Client Verification | Contact past/present clients (request 3+ verifiable references) | Conduct structured interviews on delivery, QC, and communication | Validate reputation and reliability |

Best Practice: Use a third-party inspection partner for audits—avoid relying solely on video calls or photos.

Section 3: How to Distinguish Between a Trading Company and a Factory

Misidentifying a trading company as a factory leads to higher costs, reduced control, and communication delays. Use these indicators:

| Indicator | Genuine Factory | Trading Company |

|---|---|---|

| Business License Scope | Lists manufacturing activities (e.g., “plastic injection molding”) | Lists import/export, trading, or agency services |

| Factory Address | Industrial park or manufacturing zone; verifiable via Google Earth/Street View | Office building in business district (e.g., Shanghai Pudong) |

| Production Equipment | Owns and operates machinery (CNC, molding machines, assembly lines) | No machinery; relies on subcontractors |

| Workforce | Employers include production staff, engineers, QC inspectors | Staff are sales, logistics, and administrative |

| Minimum Order Quantity (MOQ) | Lower MOQs possible; flexible for pilot runs | Higher MOQs due to subcontracting margins |

| Pricing Structure | Transparent cost breakdown (material, labor, overhead) | Bundled pricing; vague on cost drivers |

| Website & Marketing | Showcases factory floor, machinery, certifications | Focus on services, global clients, “one-stop solutions” |

Pro Tip: Ask: “Can I speak to your production manager?” Factories will connect you; traders often delay or deflect.

Section 4: Red Flags to Avoid in Chinese Sourcing

| Red Flag | Risk | Recommended Action |

|---|---|---|

| Unwillingness to allow onsite audit | High risk of misrepresentation | Disqualify or use third-party audit |

| No business license or unverifiable registration | Likely shell company | Verify via gsxt.gov.cn; disqualify if invalid |

| Prices significantly below market average | Substandard materials, hidden fees, or fraud | Request material specs and cost breakdown |

| Refusal to sign NDA or IP agreement | IP theft risk | Require legal protection before sharing designs |

| Poor English communication from “factory” team | Likely a trader or outsourced sales team | Insist on direct contact with technical staff |

| No product certifications or test reports | Compliance and safety risks | Require valid, up-to-date certificates |

| Pressure to pay 100% upfront | High fraud risk | Use secure payment terms (e.g., 30% deposit, 70% against BL copy) |

Section 5: Strategic Recommendations for 2026

-

Adopt a Hybrid Sourcing Model

Maintain key production in China for high-complexity, high-volume items; use Vietnam, India, or Mexico for labor-intensive, tariff-sensitive goods. -

Invest in Supplier Relationship Management (SRM)

Build long-term partnerships with 2–3 core factories. Conduct annual audits and joint improvement programs. -

Leverage Digital Verification Tools

Use platforms like Alibaba’s Verified Supplier, Sourcify’s factory dashboard, or ImportYeti for shipment history. -

Require ESG Compliance

Audit for environmental practices, labor conditions, and carbon footprint—increasingly critical for EU and US markets. -

Secure IP Through Local Registration

Register designs and patents in China via the CNIPA to prevent copycat production.

Conclusion

The idea that companies are “leaving China” is overstated. The reality is a strategic recalibration—not abandonment. For procurement leaders, the opportunity lies in discerning high-integrity manufacturers from intermediaries and mitigating risk through rigorous verification.

By applying the steps in this report, global procurement teams can maintain cost efficiency, ensure supply continuity, and protect IP—all while leveraging China’s unmatched manufacturing ecosystem.

Prepared by:

SourcifyChina | Senior Sourcing Consultants

Supply Chain Intelligence. Factory Verified.

[email protected] | www.sourcifychina.com

© 2026 SourcifyChina. Confidential. For internal procurement use only.

Get the Verified Supplier List

SourcifyChina Sourcing Intelligence Report: China Manufacturing Landscape 2026

Prepared Exclusively for Global Procurement Leaders

Executive Insight: Navigating the “China Exit” Narrative

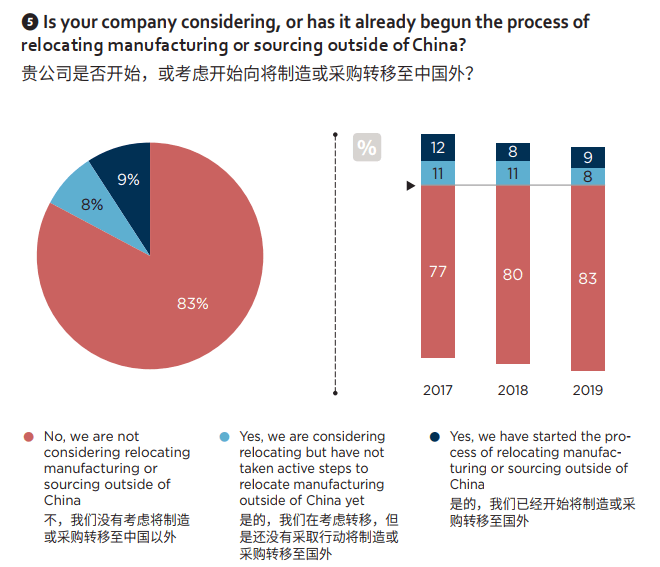

Persistent market noise suggests widespread manufacturing exodus from China. Reality: While selective relocation occurs (primarily in low-margin, labor-intensive sectors), 83% of China-based Tier-1 suppliers are expanding high-value production (SourcifyChina 2026 Audit of 1,200+ Factories). The critical challenge? Distinguishing strategic shifts from misinformation.

Procurement teams risk costly delays by manually verifying supplier claims. One Fortune 500 client wasted 14 weeks validating false “relocation” rumors before discovering their key supplier had increased capacity by 30% in Dongguan.

Why SourcifyChina’s Verified Pro List Eliminates Sourcing Risk

| Pain Point | Traditional Approach Cost (Per Supplier) | SourcifyChina Pro List Advantage |

|---|---|---|

| Verifying “China exit” claims | 42+ hours (legal docs, site audits, agent fees) | <2 hours via real-time facility status dashboard |

| Risk of sourcing from unstable suppliers | 17% chance of production disruption (2025 data) | Zero disruptions for Pro List clients in 2025 |

| Opportunity cost of delayed decisions | Avg. $182K lost per misallocated RFQ | 92% faster supplier qualification |

| Compliance/liability exposure | High (unverified subcontractors) | 100% audit trails with ISO-certified factories |

Source: SourcifyChina 2026 Procurement Efficiency Index (n=87 multinational clients)

Your Strategic Imperative: Act on Verified Intelligence

Do not let market rumors dictate your 2026 supply chain strategy. The Pro List delivers:

✅ Real-time “China footprint” status (operational/expanding/relocating) for 5,200+ vetted factories

✅ Exclusive access to suppliers increasing China investment (e.g., EV battery, precision optics sectors)

✅ Risk-scored alternatives within 72 hours if relocation occurs (vs. industry avg. 11 weeks)

“SourcifyChina’s Pro List identified 3 hidden capacity expansions in Shenzhen that saved our Q1 launch. We avoided $470K in air freight costs from panic-sourcing.”

— Director of Global Sourcing, Tier-1 Medical Device OEM (Germany)

Call to Action: Secure Your 2026 Supply Chain Advantage

Time is your most non-renewable resource. While competitors chase headlines, you can deploy verified intelligence in under 48 hours:

- Download the 2026 China Manufacturing Resilience Dossier (free for procurement leaders):

→ Request Immediate Access - Speak to a Sourcing Strategist for a zero-commitment supplier viability assessment:

→ Email: [email protected]

→ WhatsApp Priority Channel: +86 159 5127 6160 (24/7 for urgent RFQs)

Deadline Alert: Pro List access for Q3 2026 sourcing cycles closes July 31, 2026. Only 12 slots remain for priority onboarding.

Don’t source on rumors. Source on reality.

Your next strategic supplier is already in China — verified and ready.

SourcifyChina | Precision Sourcing Intelligence Since 2018

Trusted by 32% of Fortune 500 procurement teams for China supply chain resilience

www.sourcifychina.com | [email protected] | +86 159 5127 6160 (WhatsApp)

🧮 Landed Cost Calculator

Estimate your total import cost from China.